Money’s Many Names

What Founders Miss About Capital, Power, and Startup Survival

Money is never just money.

That is the first illusion of entrepreneurship. Inexperienced founders look at a balance sheet and see dollars as fixed units. They treat capital as if it has one identity, one purpose, and one moral weight. Raise it. Spend it. Track it. Repeat.

But money changes meaning every time the context changes.

In school, it is called a fee.

In divorce, it becomes alimony.

In court, it turns into fines.

To kidnappers, it is ransom.

In marriage, it may be called dowry.

When you owe someone, it is debt.

When you pay the government, it is a tax.

To retirees, it becomes a pension.

From employer to worker, it is salary.

From master to subordinate, it is wages.

In a temple or church, it is donation.

When borrowed from a bank, it is a loan.

After good service, it becomes tips.

When illegally received in the name of service, it is a bribe.

The amount may be the same. The function is not.

That is more than a language lesson. It is a foundational lesson.

Because inside every startup, money changes its name too. As a company moves from idea to product, from product to organization, and from organization to institution, capital changes character. The best founders are not simply good at raising money. They are good at understanding what that money has become.

That is where judgment lives. That is where discipline lives. That is where companies survive or quietly come apart.

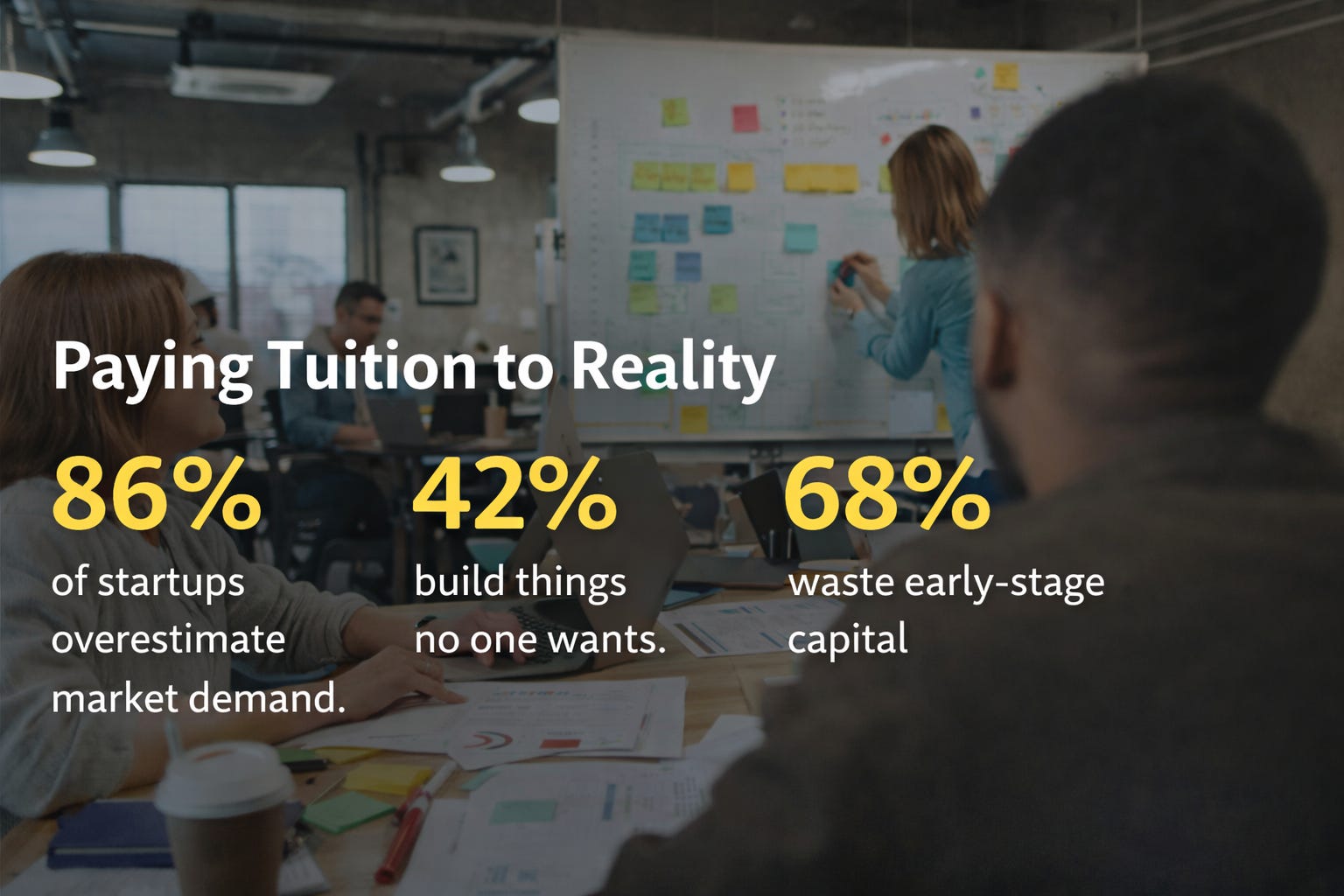

1. At the beginning, capital is a fee

Every serious company begins by paying tuition to reality.

Not to a university. To the market.

In the earliest stage, capital is not fuel for scale. It is a fee for learning. A fee for discovery. A fee for the uncomfortable education of finding out whether your idea matters to anyone outside your own imagination.

This is where inexperienced founders make their first category mistake. They treat early money like validation when it is really education. They think the raise proves the business. It does not. It only buys the right to keep testing.

The first dollars in a startup should buy understanding:

conversations with customers

rapid prototypes

product iteration

distribution experiments

the right to be wrong early and cheaply

In this phase, undisciplined spending is not just wasteful. It is presumptuous. It assumes the company already knows what it is doing.

It usually does not.

The strongest founders understand that early capital is a fee paid to remove illusion. Every dollar should reduce confusion. Every experiment should sharpen truth. Every month should make the market more legible.

If it does not, then the money was not an investment. It was tuition with no lesson learned.

So many young companies fail in such a familiar way. They do not die because they lack energy. They die because they spent before they understood.

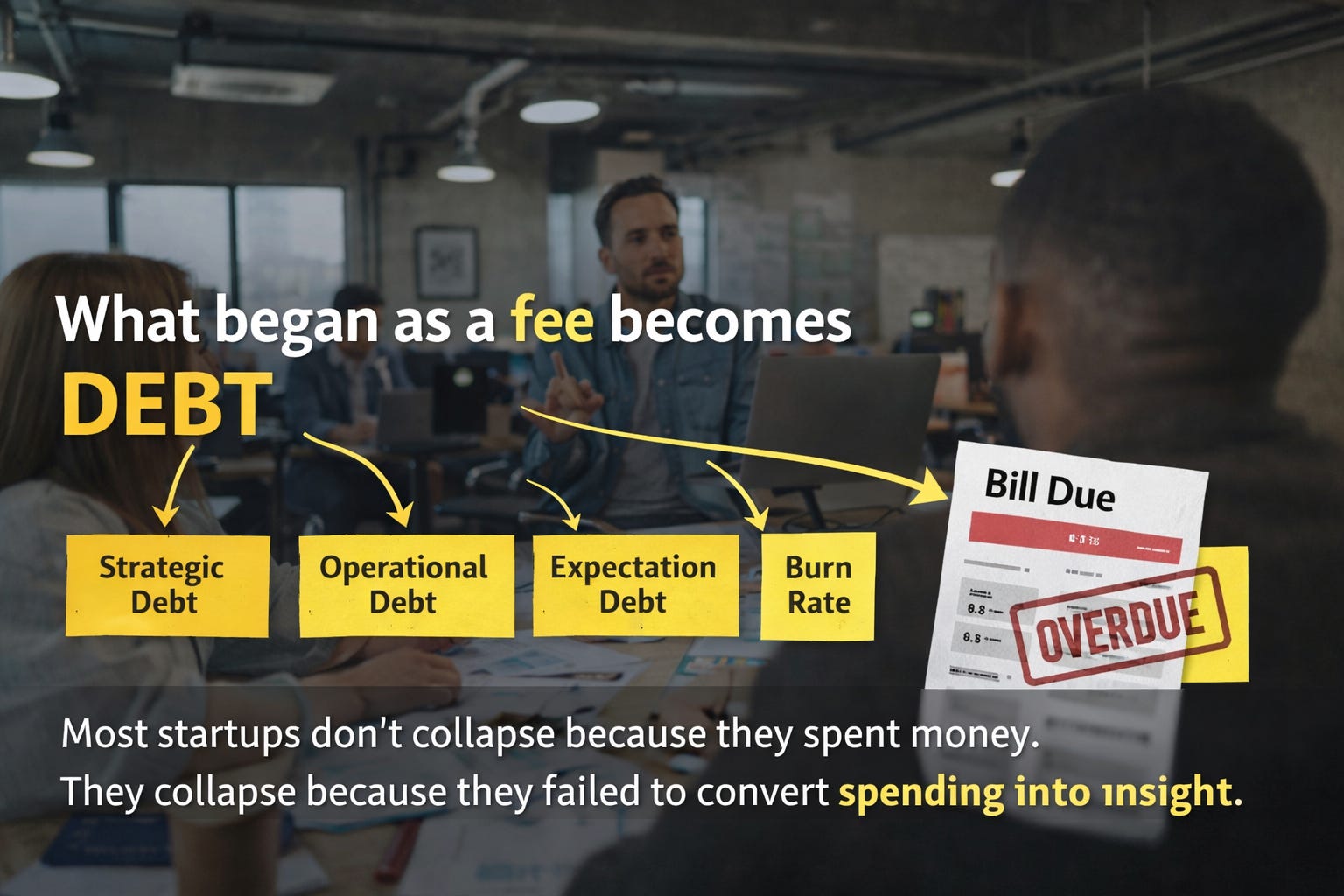

2. Left unmanaged, a fee becomes debt

Most startups do not collapse because they spent money. They collapse because they failed to convert spending into insight.

That is when money changes its name.

What began as a fee becomes debt.

Not always legal debt. Not always bank debt. But strategic debt. Operational debt. Expectation debt.

You raised capital. Now the future expects something from you.

You hired before clarity. That creates debt. You promised growth before fit. That creates debt. You scaled systems before demand. That creates debt. You accepted confidence from investors and failed to turn it into traction. That creates debt.

A founder does not escape obligation simply because the check came as equity instead of a loan. The spreadsheet may classify it one way. Reality often classifies it another.

There is always a bill.

Sometimes it arrives as a dilution. Sometimes as burnout. Sometimes as emergency bridge financing. Sometimes as a down round. Sometimes as the slow humiliation of discovering that months of motion produced almost no real progress.

This is why mature founders respect early money. They know every dollar carries a shadow. If the company fails to turn capital into learning, momentum, or leverage, that shadow grows.

A startup can survive being underfunded. Many do. It rarely survives being overconfident with borrowed time.

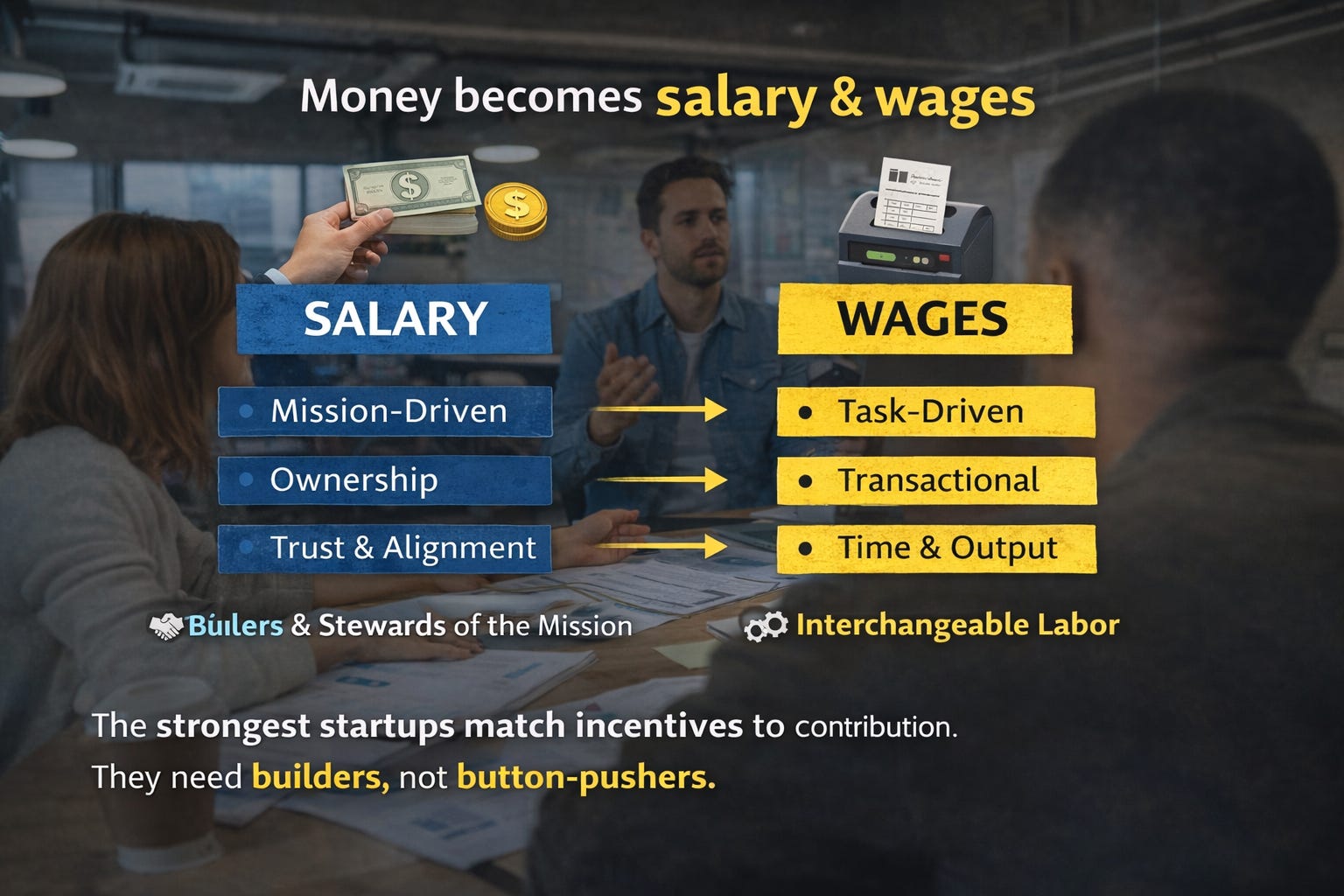

3. As a company grows, money becomes salary and wages

Once a company moves beyond its first fragile experiments, capital changes again.

Now it is no longer mostly about learning. It is about organizing human effort.

That is where money splits into two very different forms: salary and wages.

On paper, the distinction looks administrative. In practice, it reveals something deeper about how a company thinks.

Salary implies continuity, trust, and responsibility. It suggests that someone is being paid not merely to complete isolated tasks, but to carry part of the mission.

Wages are more transactional. Time given. Task completed. Payment delivered.

A healthy company needs both. That is not the problem.

The problem begins when founders confuse the two, or worse, ask for ownership-level commitment while treating people as interchangeable labor.

You cannot ask for creativity, resilience, judgment, and loyalty from people while structuring the relationship as if they are temporary inputs. If your language says mission but your incentives say transaction, people notice. Culture notices. Talent notices.

And once the best people notice, they begin to detach.

The strongest startups know how to match incentives to the kind of contribution they truly need. Some roles require more than output. They require stewardship. They require people who can make decisions under uncertainty. They require builders, not button-pushers.

That usually demands more than money alone. It demands trust, autonomy, clarity, and sometimes ownership.

Payroll is not just an expense line. It is a philosophy made visible.

4. Success eventually invites tax

As long as a company is small, it can romanticize freedom.

It can move fast, ignore ceremony, improvise process, and celebrate its lack of bureaucracy. In the beginning, this feels like an advantage. Often it is.

Then scale arrives.

And scale changes the name of money again.

Now some of it becomes tax.

Success creates obligations. Legal ones. Structural ones. Administrative ones. Reputational ones.

More customers mean more scrutiny. More markets mean more regulation. More visibility means more accountability. More influence means less room for sloppiness disguised as genius.

Immature founders experience this as persecution. Mature founders understand it as the price of entering a larger arena.

Every serious company eventually pays a tax for legitimacy.

Compliance is a tax. Governance is a tax. Security is a tax. Auditability is a tax. Professionalization is a tax.

The point is not to resent these costs. The point is to see them early enough that they do not come as a surprise.

Many promising startups break here. They know how to invent but not how to institutionalize. They know how to generate velocity but not how to carry weight.

That is when the market stops treating them like insurgents and starts asking whether they can behave like infrastructure.

5. Poor judgment turns tax into fines

There is a difference between the cost of scale and the penalty for irresponsibility.

That is the difference between tax and fines.

Tax is the normal burden of operating in the real world. Fines are what happen when you refuse to respect it.

This distinction matters more than founders think.

A company that invests in governance, contracts, compliance, financial discipline, and operational maturity is paying tax. A company that ignores those responsibilities until regulators, courts, partners, or reality intervene is paying fines.

One is the cost of adulthood. The other is the price of denial.

Startup culture has a habit of romanticizing recklessness. It calls it boldness. It calls it founder mode. It calls it disruption. But very often it is simply a deferred consequence.

You can ignore the process for a while. You cannot ignore consequences forever.

This is why the best founders do not just ask, “How fast can we move?” They also ask, “What liabilities are we creating while moving this fast?”

That is the better question. It is often more expensive in the short term. It is almost always cheaper in the long term.

6. Some legacy obligations resemble alimony

Not every past commitment remains useful forever.

A co-founder relationship changes. An early partnership becomes misaligned. A vendor contract outlives its value. A strategic direction that once made sense becomes dead weight.

In business, these moments rarely end cleanly.

And that is where money can begin to resemble alimony.

Not literally. Structurally.

It becomes the ongoing cost of an earlier arrangement that no longer fits the future.

This is one of the quieter truths of company building. Founders love origin stories. They love loyalty, mythology, and the romance of the garage. But companies evolve unevenly. People evolve unevenly. Incentives drift.

Sometimes the future requires separation.

That separation usually costs money:

buyouts

legal settlements

transition packages

restructuring costs

the long tail of old promises

The mistake is not that these costs exist. The mistake is pretending they do not.

A founder who refuses to deal with outdated commitments often pays twice. Once in money. And again in lost momentum.

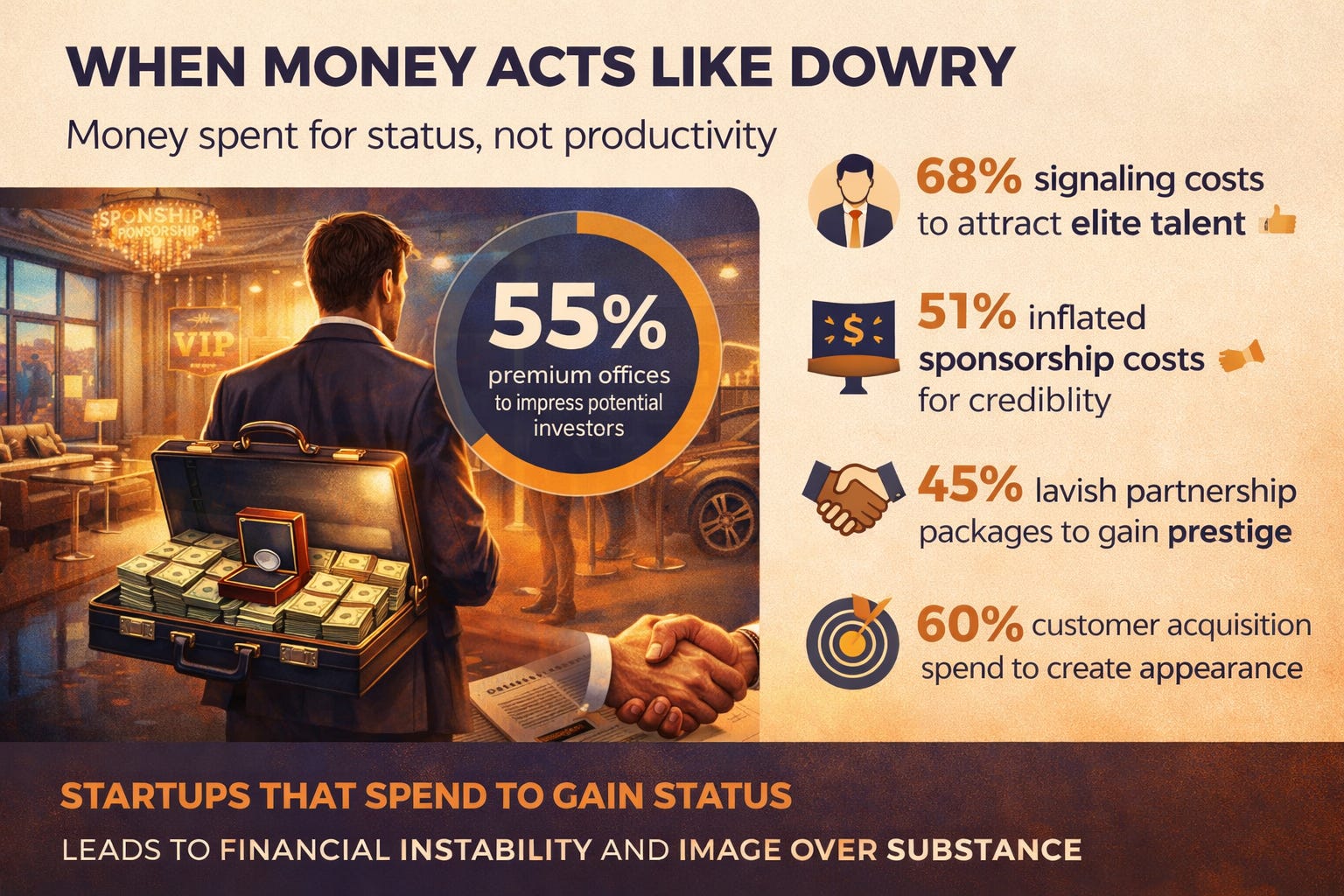

7. In some companies, capital starts acting like a dowry.

This is uncomfortable territory, which is one reason it matters.

Sometimes money is not deployed for productivity at all. It is deployed for acceptance. For admission. For status.

That is when capital starts acting like dowry.

Not literally. Strategically.

It is money used to gain entry into relationships or rooms that might otherwise stay closed.

In startups, this can take familiar forms:

costly signaling to attract elite talent

extravagant offices to impress investors

inflated sponsorships to buy proximity

lavish partnership terms offered for credibility

expensive customer acquisition designed less to build loyalty than to manufacture appearance

Some of this is normal. Markets do run on perception. But perception can become addictive. And once a company starts paying for status instead of substance, the economics begin to rot from the inside.

The best founders know the difference between strategic signaling and expensive insecurity.

One opens doors. The other quietly empties the room.

8. At maturity, great companies create pension-like trusts.

Inside a startup, the closest equivalent to a pension is not retirement. It is institutional trust.

A great company eventually reaches a point where money is no longer just buying effort for today. It is reinforcing confidence in tomorrow.

Employees stay because they trust the company will endure. Customers commit because they trust the company will keep delivering. Partners align because they trust the company will remain credible. Investors support because they trust management will allocate capital intelligently.

This is pension-like money. Money as long-horizon reassurance. Money as stability. Money as evidence that the enterprise is durable enough to support lives beyond this quarter.

Very few startups reach this stage. Many never should. But the ones that do stop feeling like speculative projects and start feeling like institutions.

That transition is profound.

It means capital is no longer just chasing growth. It is underwriting continuity.

9. In healthy ecosystems, money becomes donation

The most respected companies eventually learn that not every dollar should be optimized for immediate extraction.

At a certain stage, some capital must flow outward.

That is where it becomes a donation.

A company donates to its ecosystem when it contributes beyond direct self-interest:

sharing knowledge

supporting open standards

investing in community

mentoring founders

funding public goods in its category

helping build the market it benefits from

This is not softness. It is not charity theater. It is often strategic wisdom.

The strongest firms understand that ecosystems do not sustain themselves. Someone has to maintain trust. Someone has to strengthen the surrounding environment. Someone has to create the conditions in which talent, ideas, standards, and opportunity can circulate.

Short-term thinkers see the process as a waste. Long-term builders see it as architecture.

In the best cases, donation is how power matures. It stops merely taking from the system and starts reinforcing the system that made its success possible.

10. In weak hands, money becomes a bribe.

Every founder should spend serious time thinking about this word.

Bribe is the darkest name money wears, and in business it does not need to be literal to be dangerous.

Sometimes money functions like a bribe even when no law is broken.

It becomes a bribe when it is used to purchase appearances that have not been earned.

Buying engagement instead of building relevance. Subsidizing retention that would vanish at true market pricing. Overpaying for distribution to create the illusion of pull. Manufacturing momentum that the product itself cannot sustain. Inflating vanity metrics so outsiders confuse motion for strength.

This is one of the central temptations of startup life. Markets reward narrative. Capital amplifies narrative. Software makes weak traction look polished. Distribution can be rented. Attention can be engineered. For a while, almost anything can be made to look inevitable.

But illusion is expensive.

Eventually the numbers have to stand on their own. Eventually the company has to function without artificial support. Eventually the market asks the only question that matters:

Would this business still stand if the subsidy vanished?

If the answer is no, then the company may not be scaling. It may simply be bribing reality to stay quiet for one more quarter.

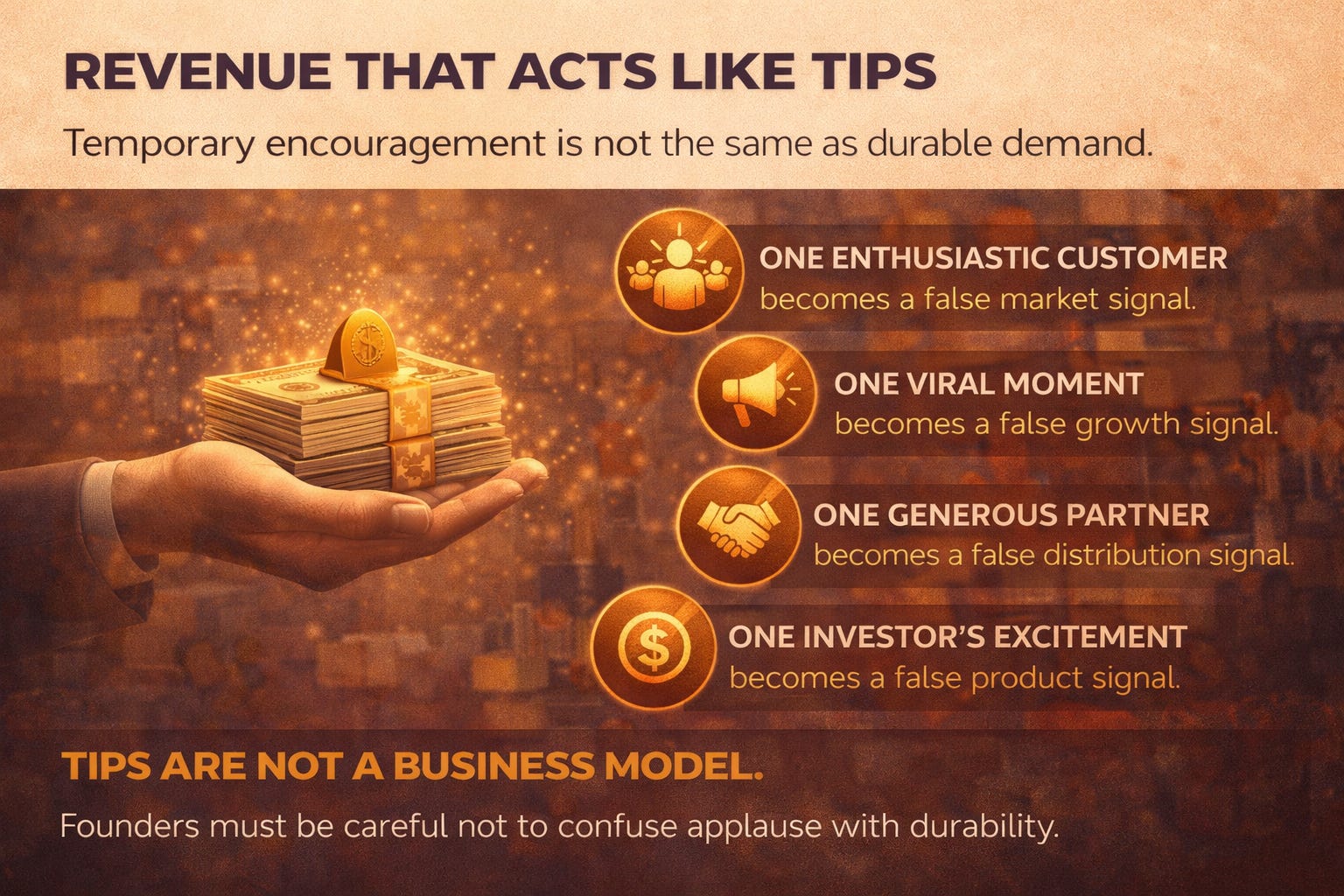

11. Sometimes founders mistake momentum for tips

After good service, money becomes tips. For founders, this is a useful warning.

Some revenue is not durable demand. It is encouragement. It is a novelty. It is curiosity. It is goodwill. It is people rewarding effort before the value proposition is fully proven.

That can be helpful. But it can also be misleading.

A founder who mistakes early enthusiasm for repeatable economics will build a fantasy on top of a courtesy.

This happens all the time:

one enthusiastic customer becomes a false market signal

one viral moment becomes a false growth signal

one generous partner becomes a false distribution signal

one investor’s excitement becomes a false product signal

Tips are not a business model.

They are a clue. Sometimes a gift. Sometimes a temporary grace period. But founders must be careful not to confuse applause with durability.

12. Borrowed capital is still a loan

No founder should lose sight of this emotional truth.

Even when money does not come from a bank, it often behaves like borrowed expectation.

Capital buys time. It buys optionality. It buys people, experiments, reach, infrastructure, and retries.

But above all, it buys time.

And time is not free.

One of the deepest mistakes in startup culture is not overspending. It is forgetting that outside capital compresses time. Every dollar comes with an invisible clock attached to it. Some clocks are contractual. Some are reputational. Some are psychological. All of them matter.

Fundraising should never be mistaken for escape. In many cases it is simply the beginning of a louder countdown.

13. At the extreme, success itself can feel like ransom

There is one final transformation the best founders eventually encounter.

At first, they want freedom. That is often why they build.

Then the company grows. Investors enter. Employees depend on it. Customers expect continuity. The market develops opinions. The board develops leverage. The press develops narratives. The founder becomes symbol, operator, diplomat, and prisoner of consequence all at once.

And that is when money can begin to feel like ransom.

Not because success is bad. Because scale creates hostages.

Your time gets taken. Your optionality narrows. Your identity fuses with the company. Your decisions become public property. Your freedom becomes expensive again.

The irony is brutal. Many founders start companies to become free, only to discover that a successful company can become its own kind of captivity.

That is why the wisest builders do not just ask how to win. They ask what victory will demand from them once it arrives.

That question is rarer. And usually more important.

The real lesson

Money changes names because life changes relationships.

That is the truth hiding in entrepreneurship.

The same dollar can educate or distort. It can align or exploit. It can strengthen a system or conceal a weakness. It can liberate or trap. It can be proof of value or camouflage for its absence.

Founders who treat all money the same usually end up misallocating it. They spend growth capital like tuition. They spend trust as if it were infinite. They subsidize illusion and call it strategy. They resent the tax of maturity and then act shocked by the fines. They confuse wages for loyalty, tips for traction, loans for validation, and bribes for momentum.

The sharpest founders do something different.

Before every major decision, they ask a simple question:

What is this money called now?

Because if you can answer that honestly, you are far less likely to waste it.

And in the end, that may be the real edge.

Not the ability to raise more. Not the ability to spend faster. Not the ability to look bigger than you are.

The real edge is semantic discipline. The ability to recognize that money has changed its name before it changes your company.

Ken, amazing article as usual. "What is this money called now?" is a question most founders never think to ask. That reframe alone is worth the whole read.