The Empty Bourse and the Diamond Seed

In Surat, India, a building built for certainty now sits inside an industry defined by doubt.

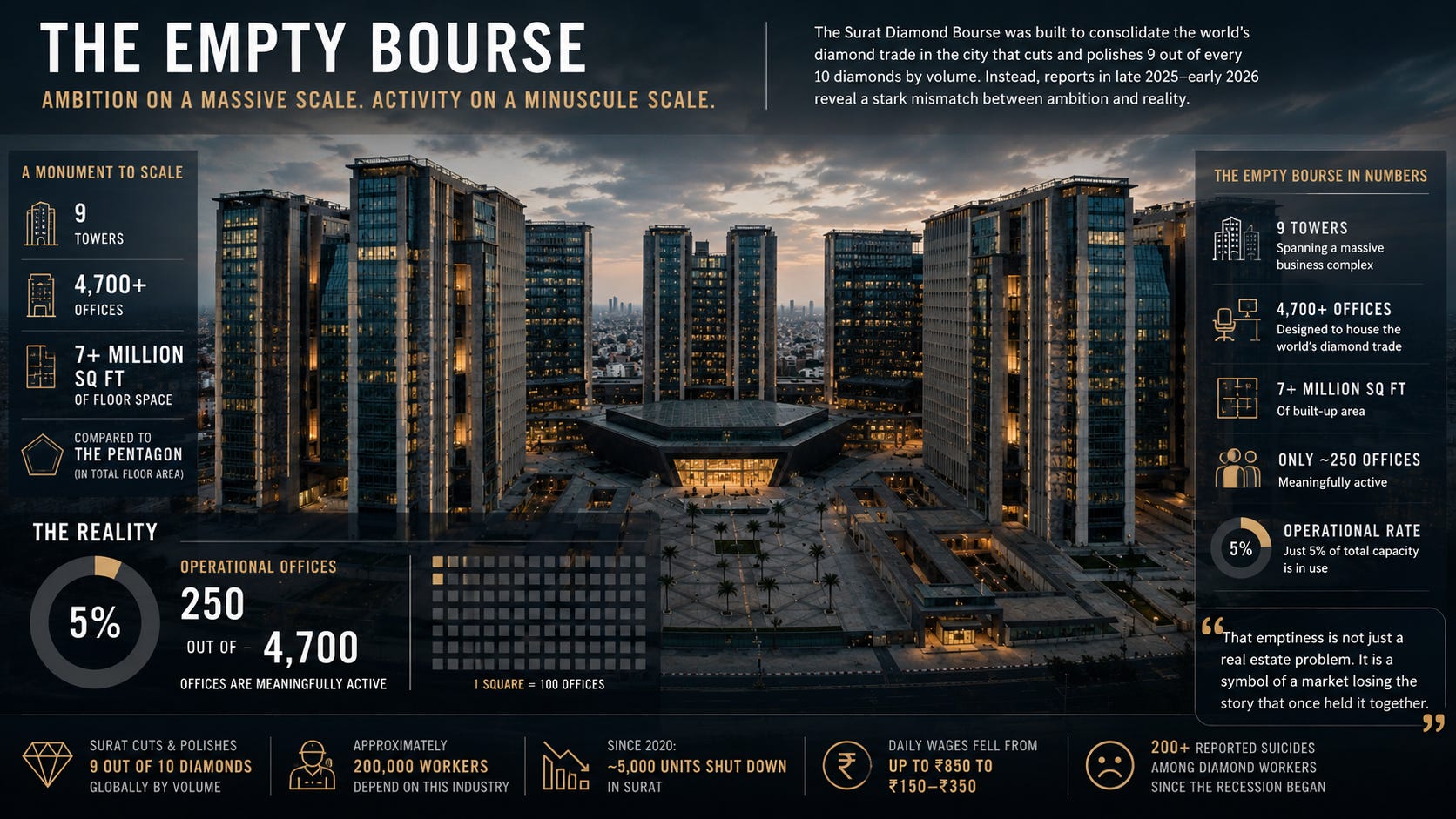

The Surat Diamond Bourse was designed as a monument to scale: nine towers, thousands of offices, and more than 7 million square feet of floor space. By total floor area, it has been widely compared to the Pentagon. It was supposed to consolidate the world’s diamond trade in the city that already cuts and polishes the overwhelming majority of the planet’s diamonds by volume. Instead, reports through late 2025 and early 2026 describe a strange mismatch between ambition and reality: thousands of offices, but only a small fraction is meaningfully active. According to a bourse spokesperson, reports put the number of operational offices around just 250 out of 4,700.

That emptiness is not just a real estate problem. It is a symbol of a market losing the story that once held it together.

For more than a century, diamonds were sold as nature’s perfect scarcity. Ancient. Finite. Romantic. Formed deep under the Earth over impossible time, then placed on a finger as proof of devotion.

But the modern diamond business was never built on geology alone. It was built on control.

De Beers understood this better than anyone. At its peak, the company controlled the overwhelming majority of the world’s rough diamond distribution, using its famous campaigns to manufacture a social norm that linked romantic commitment to a stone. It stockpiled inventory, rationed supply, and sold through a tightly managed system of “Sights,” where selected buyers received pre-allocated boxes at non-negotiable prices set by the company. It was not a normal commodity market. It was a theater of scarcity, disciplined enough to make abundance feel rare.

How De Beers Controlled The Diamond Industry For 100 Years

A historical context on how De Beers engineered scarcity and built one of the most successful monopoly structures in modern business history. It strengthens the reader’s understanding of the article’s core thesis before the lab-grown disruption begins.

Then the laboratory learned how to grow the stone.

Chemical Vapor Deposition, or CVD, changed the emotional math. Inside a controlled vacuum chamber, plasma is ignited from hydrogen and hydrocarbon gases such as methane. Carbon atoms break down and collect layer by layer on a single-crystal diamond seed.

The result is not cubic zirconia or glass. It is a diamond, with the same core crystal lattice, hardness, and chemical identity as a mined stone. While specialized laboratory equipment can still identify growth origin, the traditional consumer distinction between “real” and “fake” has become commercially harder to defend.

That was the rupture. Once a buyer could purchase a nearly indistinguishable diamond for a fraction of the price, the industry’s most important sentence began to weaken:

“A diamond is forever.”

Forever started to sound expensive.

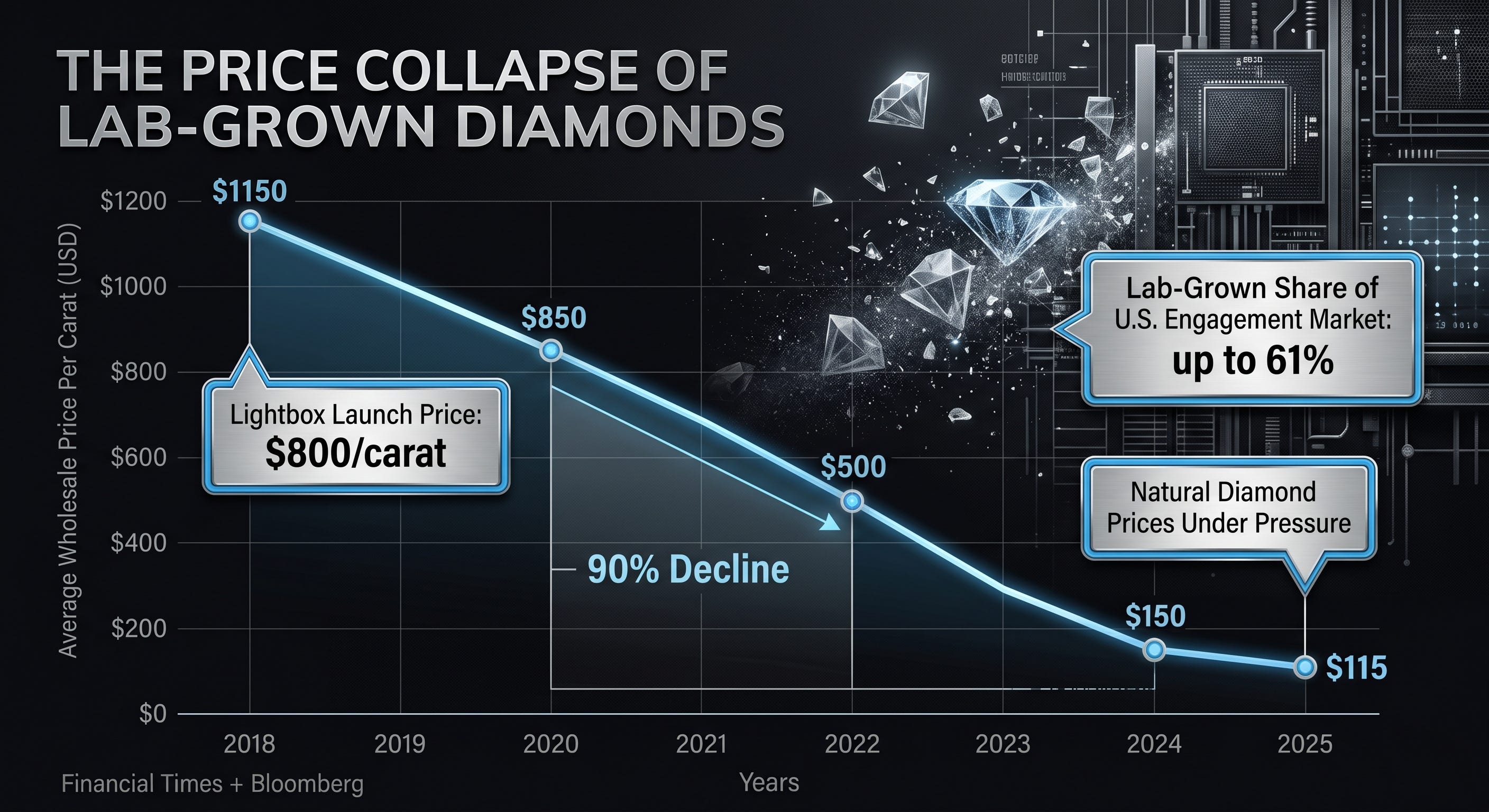

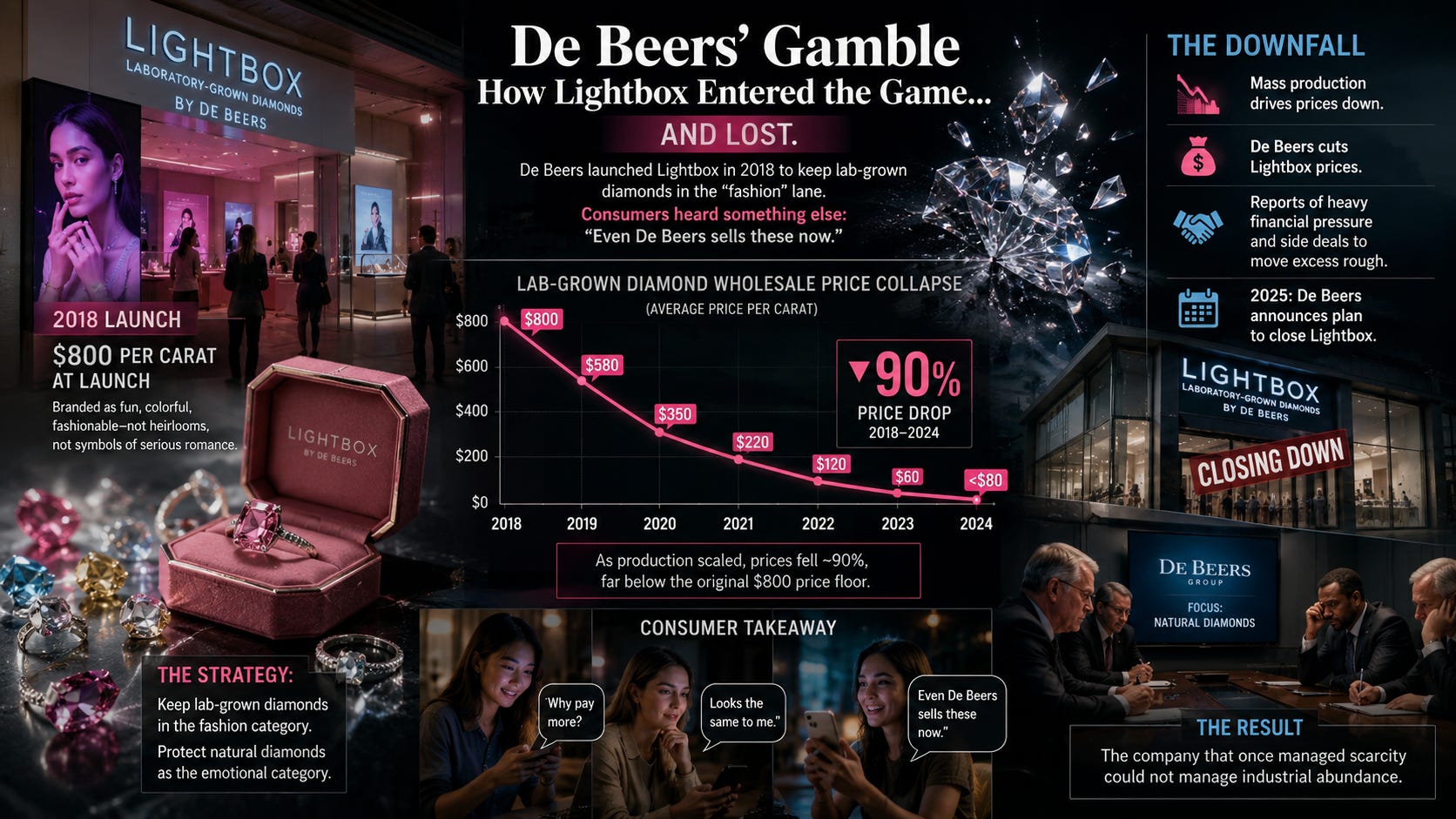

De Beers tried to contain the threat in 2018 with Lightbox, its lab-grown jewelry brand. The pricing was deliberately blunt: $800 per carat at launch. The branding was just as calculated. Lab-grown stones were presented as fun, colorful, and fashionable, but not as heirlooms. Not as symbols of serious romance.

The strategy made sense on paper. Keep lab-grown diamonds in the fashion category. Protect natural diamonds as the emotional category. But consumers do not always receive the message a company thinks it is sending.

By entering the category, De Beers validated it. Many buyers did not hear, “This is not a real diamond.” They heard, “Even De Beers sells these now.”

Then the economics ran away from them. Lab-grown wholesale prices collapsed by an estimated 90% between 2018 and 2024 as production scaled, eventually dropping far below the original $800 price floor. De Beers cut Lightbox prices, reported heavy financial pressure, moved excess rough stock through quiet side deals, and by 2025 had announced its intention to close Lightbox and focus again on natural diamonds.

The company that once managed scarcity could not manage industrial abundance.

The damage became visible fastest in Surat.

For decades, Surat’s polishing economy thrived because it mastered the small stone. European hubs handled prestige. Surat handled volume. Family workshops, skilled polishers, brokers, exporters, and merchants turned the city into the engine room of the diamond world, processing nine out of every ten stones globally.

But a volume economy is fragile when volume slows.

Factories cut shifts. Small workshops closed. Industry and labor estimates indicate that since 2020, roughly 5,000 units have shut down, leaving an estimated 200,000 workers unemployed. Workers who had built their lives around polishing benches saw wages cut by up to half, with reported daily earnings falling from pre-crisis rates of up to ₹850 to a range of ₹150 to ₹350.

According to data from local diamond worker unions, the distress also produced a severe mental health crisis, with more than 200 reported suicides among diamond workers since the beginning of the recession. Municipal schools saw climbing dropout rates as families struggled to cover basic costs, with hundreds of children leaving classrooms behind. By March 2025, large numbers of workers were marching through Surat demanding a welfare board, salary hikes, and an urgent government relief package.

Nothing Lasts Forever (2023) Official Trailer

This documentary trailer introduces viewers to the cultural and economic disruption caused by synthetic diamonds, while also visually capturing the emotional tension inside the traditional diamond trade.

The polishing wheel is not an abstraction. It is school fees. Rent. Food. A village family’s upward mobility. When diamond demand weakens, the pain does not stop at a trading desk in Antwerp or a boardroom in London. It shows up first in the hands of the people who made the stones shine.

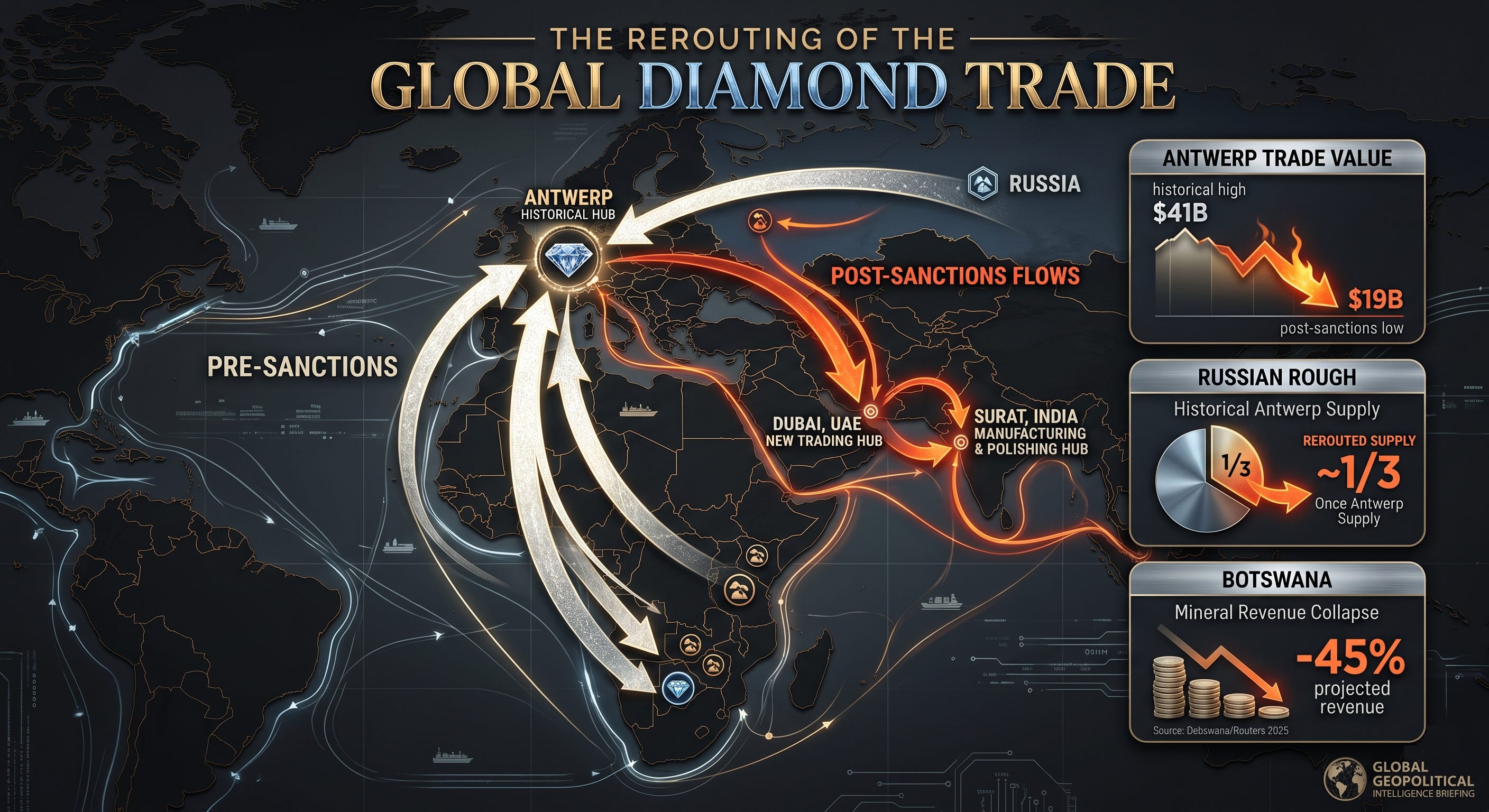

Antwerp tells the same story from another angle.

For generations, Antwerp was the capital of the rough diamond trade. But its position has weakened sharply. Total diamond trade value in the city fell from a peak of $41 billion in 2022 to about $19 billion in 2025. Sanctions on Russian diamonds, a retreat by Chinese luxury buyers, and record-high gold prices all played a role.

The G7 and Western sanctions were designed to choke off revenue from Russian rough stones, which previously made up roughly one-third of Antwerp’s supply. But diamonds, like water, find channels. The trade rerouted around Western Europe, redirecting stones toward Dubai and India, where the restrictions were easier to avoid.

The lesson was deeply uncomfortable. Sanctions can reshape global trade flows. They do not always stop them.

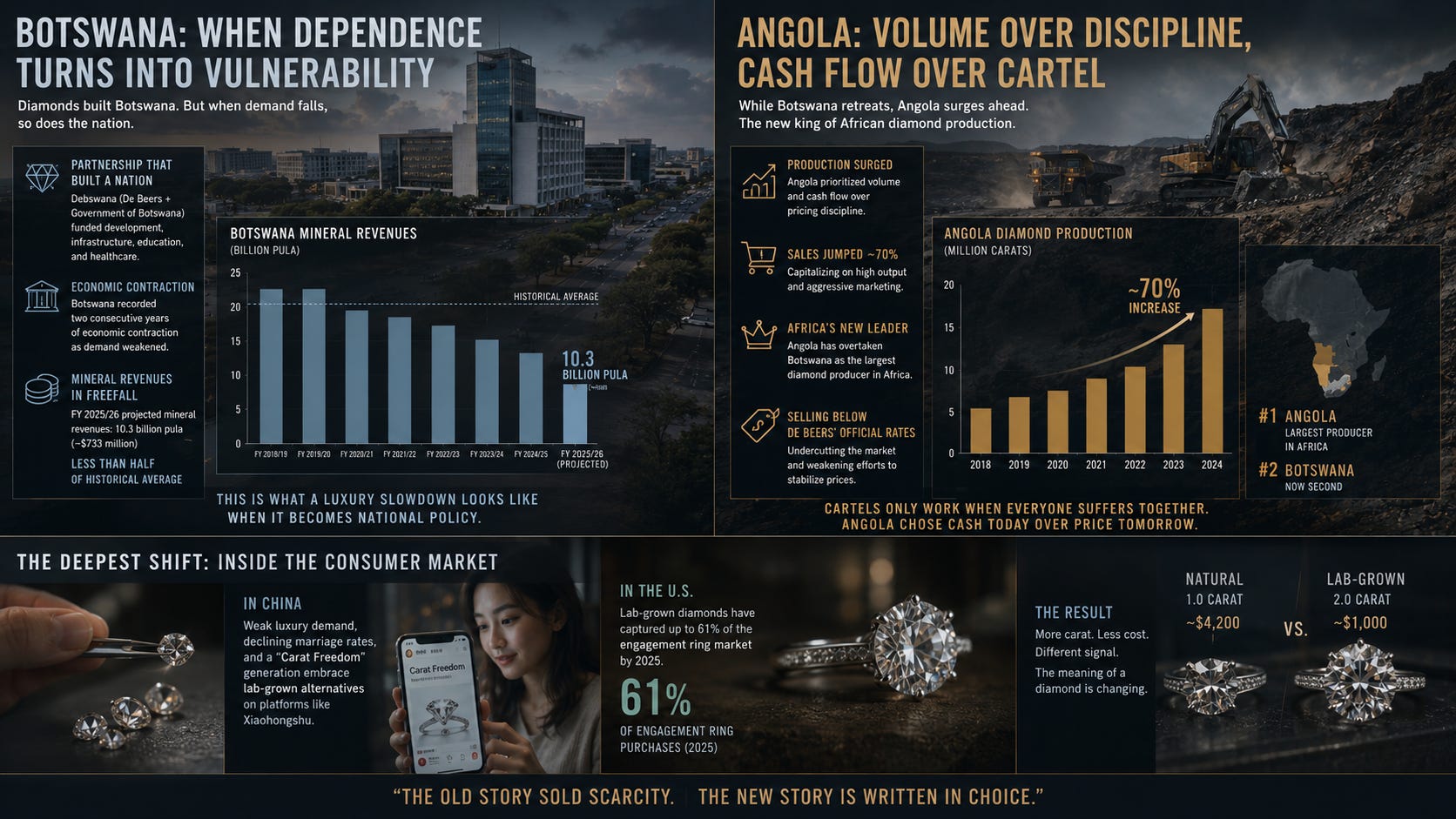

Botswana’s problem is harder still.

For decades, diamonds helped build the modern Botswanan state. The country’s partnership with De Beers through Debswana funded rapid development and public infrastructure. But diamond dependence becomes dangerous when diamond demand falls.

Facing weaker natural diamond demand, Botswana suffered two consecutive years of economic contraction, while mineral revenues for the fiscal year 2025 to 2026 were projected to fall to 10.3 billion pula, about $733 million, less than half the country’s historical average. This is what a luxury slowdown looks like when it becomes national policy.

Angola, meanwhile, has moved in the opposite direction. Rather than defending old pricing discipline or cutting supply, Angola prioritized volume and cash flow. Production surged. Sales jumped nearly 70%. The country overtook Botswana as Africa’s largest producer.

By selling below De Beers’ official rates, Angola weakened efforts to stabilize the market. Cartels only work when participants agree to suffer together. Once an outsider decides cash today matters more than price tomorrow, the old discipline starts to crack.

But the deepest shift may be happening inside the consumer market itself.

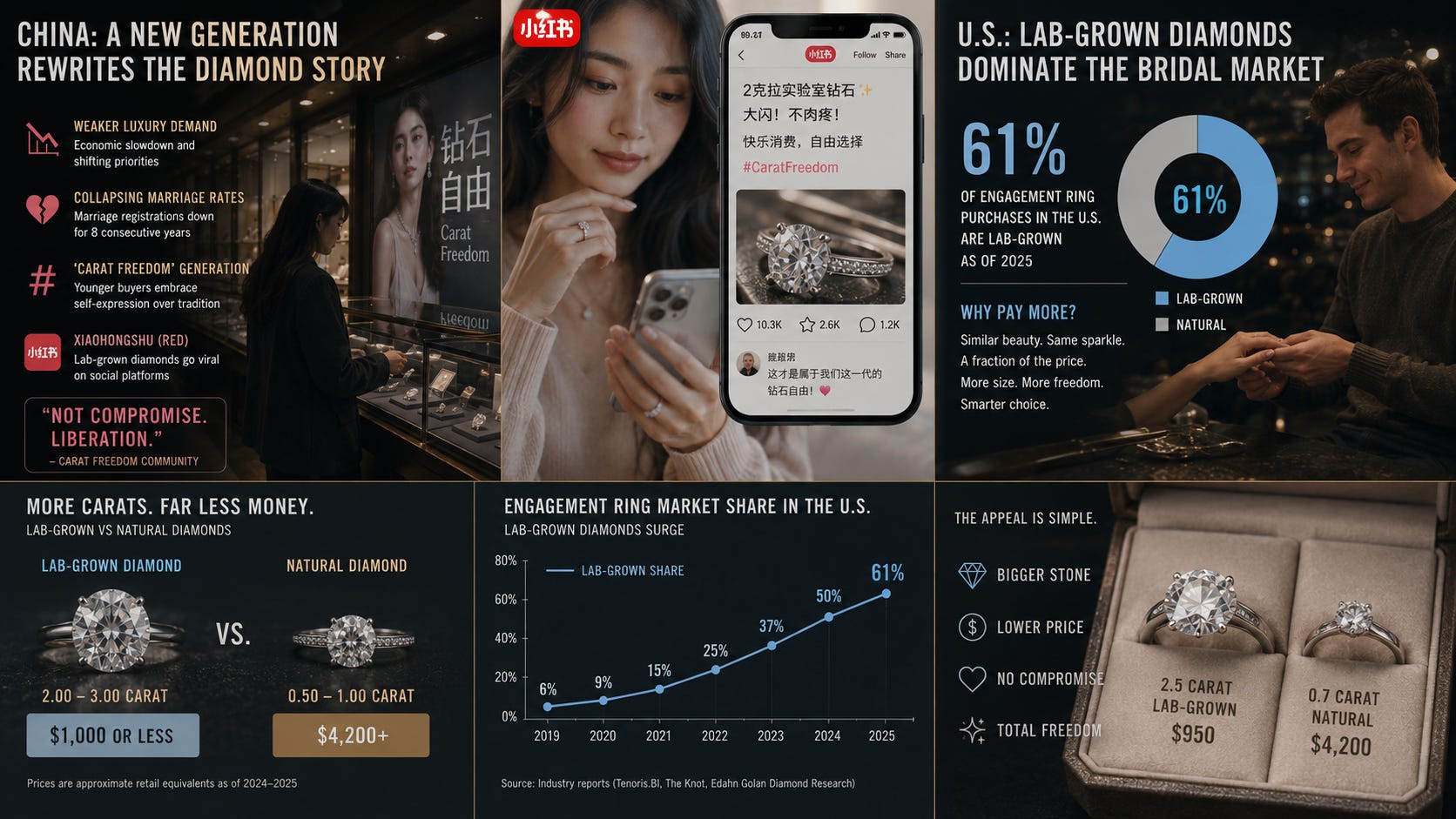

In China, the natural diamond story has been hit by weaker luxury demand, collapsing marriage rates, and a younger “Carat Freedom” generation that actively praises lab-grown alternatives on platforms like Xiaohongshu. These buyers look at a two- or three-carat synthetic stone for a fraction of the cost of a smaller natural diamond and see not compromise but liberation.

In the United States, lab-grown diamonds have captured a massive share of the bridal sector, with some industry trackers putting their share as high as 61% of engagement ring purchases by 2025. The appeal is not mysterious. Why pay a massive premium when a lab-grown alternative can cost $1,000 or less compared to a $4,200 natural equivalent?

That simple economic question created the sizing trap.

For decades, size signaled wealth. A bigger diamond meant a bigger financial sacrifice. Lab-grown diamonds scrambled that signal. As synthetic options became affordable, the average center stone size in a US engagement ring swelled from 1.31 carats in 2019 to 2.45 carats in 2025.

When larger stones became common, size stopped meaning what it used to mean. A three-carat diamond no longer automatically whispered old money or elite status. Often, it just signaled accessible technology.

That does not kill the natural diamond. It changes what the stone is for.

Approx. major WSJ feature with broad readership — This reporting deepens the article’s analysis of shifting consumer psychology, falling natural diamond prices, and the growing normalization of lab-grown stones among younger buyers.]

The market is splitting into two fundamentally different products that happen to share a crystal structure. Natural diamonds are moving toward an ultra-high-end niche, valued for geological history, authenticated provenance, and scarcity. Lab-grown diamonds are moving toward mass-market jewelry, valued for accessibility and physical perfection.

One sells geological history.

The other sells engineered precision.

The most interesting future for lab-grown diamonds may not be jewelry at all. The same atomic structure and thermal properties that make diamonds beautiful also make them increasingly important materials for 21st-century infrastructure. CVD-grown diamond plates offer thermal conductivity far above copper, making them promising substrates for high-power electronics, advanced communications systems, electric vehicles, and quantum technologies.

The stone that spent the 20th century trapped inside romance marketing may spend the 21st century driving advanced machines.

The traditional industry spent more than a century persuading the world that diamonds mattered because they were rare enough to symbolize love. Technology revealed something stranger: diamonds may become far more useful once we learn to manufacture them in abundance.

This is why the empty corridors of the Surat Diamond Bourse matter. They are not proof that diamonds are finished. They are proof that the old system of engineered scarcity is finished.

The stone survived.

The monopoly did not.