The Great Deleveraging

Identity, Industry, and Hollywood’s Audit of the Final Frontier

For years, Hollywood operated on a simple assumption: more was better. More shows. More spinoffs. More platforms. More subscriber growth at almost any cost.

That assumption shaped an era. It built the streaming wars, inflated budgets into the stratosphere, and turned legacy media companies into something they had never really been before: debt-heavy technology imitators chasing scale with the zeal of venture-backed startups. For a while, the illusion held. Wall Street tolerated the losses. Executives spoke the language of engagement, ecosystem, and lifetime value. Entire franchises were re-engineered to feed the machine.

Then the bill arrived.

What is happening now across media is not a cyclical downturn or a temporary correction. It is a deeper structural shift; a kind of corporate sobriety after a long binge. The age of Peak TV has given way to the age of the audit. Spending is no longer a proxy for ambition. Size is no longer proof of strength. The central question in Hollywood is no longer whether a company can make more content. It is whether that content can justify its existence on a balance sheet.

Nowhere is this change more visible than at Paramount.

At the intersection of Melrose and Gower, long one of Los Angeles’s symbolic crossroads of industrialized storytelling, the mood in early 2026 feels less like creative reinvention and more like financial triage. The newly formed Paramount Skydance Corporation, created after the merger that formally closed in August 2025, did not inherit a clean slate. It inherited a burden: a debt load reportedly in the range of 13.6 billion to 14.6 billion dollars, along with a business that could no longer afford the fantasies it had been telling itself.

Under Chairman and CEO David Ellison, the company’s new organizing principle is not expansion but discipline. The ambition is not to win the loudest headlines in streaming. It is to extract at least 3 billion dollars in efficiencies by 2027 and restore something more old-fashioned (and suddenly more radical): durable economics.

The Skydance-Paramount Merger: A Financial Post-Mortem An analysis of the strategic shifts and market reactions to the David Ellison-led takeover.

The End of the Walled Garden

One of the defining ideas of the streaming boom was exclusivity. Studios pulled valuable libraries off the open market and locked them inside their platforms. They believed that proprietary content would function as both moat and magnet. If a beloved franchise could drive subscriptions, then almost any cost could be rationalized as customer acquisition. A hit series was no longer just a show; it was infrastructure.

But the walled garden turned out to be an expensive religion.

By 2025, media companies were rediscovering something they had spent years trying to forget: content can be more valuable when sold widely than when hoarded defensively. Paramount’s return to licensing was not just a tactical shift. It was an admission that the old dream of self-contained streaming empires had failed to produce enough economic gravity. A successful property, especially one with global recognition, can sometimes do more work as an export than as a captive asset.

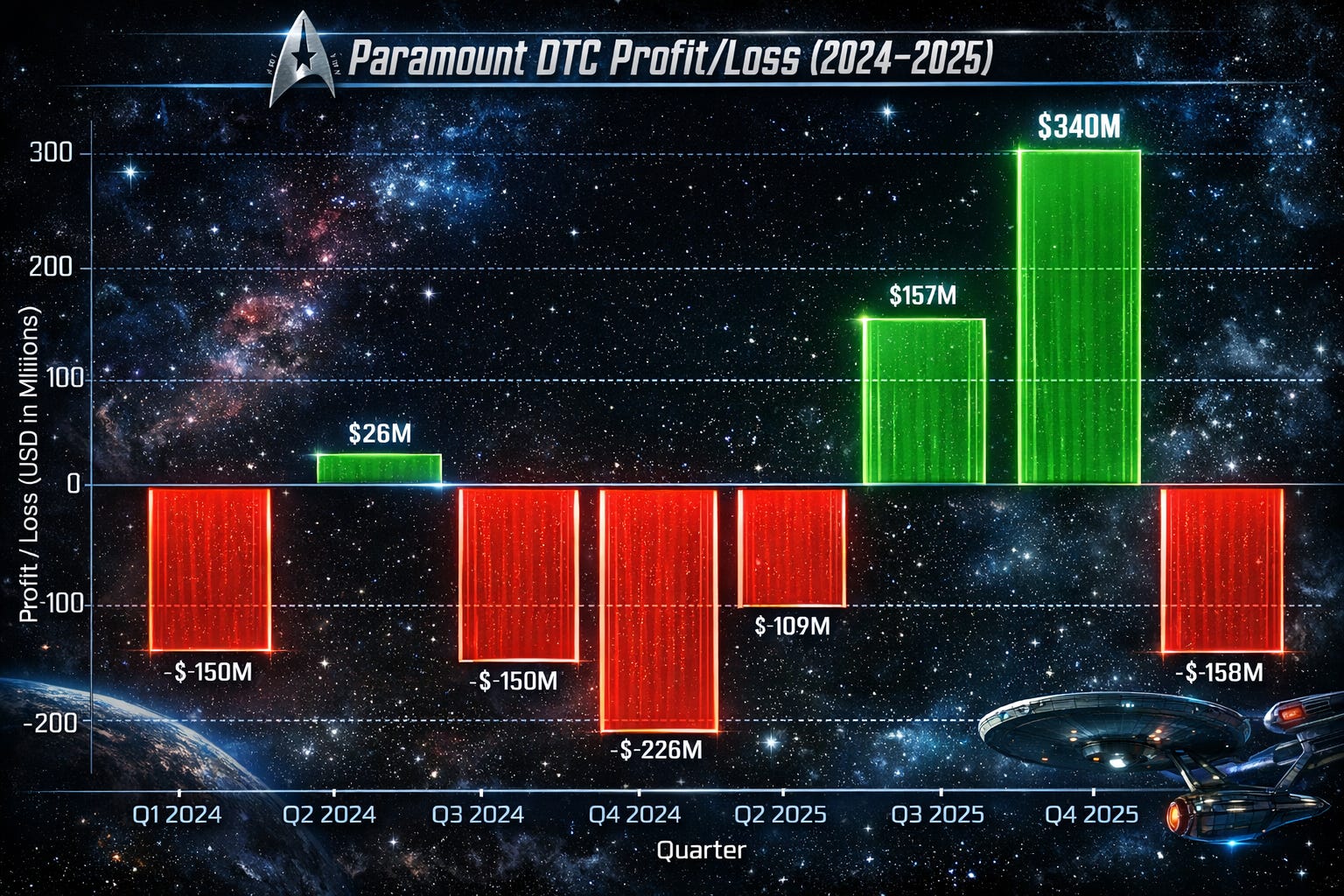

Licensing content to rivals reflects a broader industry realization that distribution purity is a luxury indebted businesses can no longer afford. In Paramount’s case, the move coincided with a reported 42% reduction in streaming losses. This was helped in part by a sharper focus on high-ARPU markets, contributing to a meaningful 340 million dollar profit in the DTC segment in the third quarter of 2025.

The streaming business is no longer being judged as a story about future scale. It is being judged as a business. And businesses cut. Late 2025 brought a first major workforce reduction of about 1,000 employees. Another 1,600 followed as Paramount shed non-core international assets. The Hollywood that wanted to be Netflix is slowly being replaced by the Hollywood that remembers it is still, underneath the jargon, a capital-intensive content business.

The Franchise Paradox

In theory, retrenchment should favor the strongest franchises. Companies tend to retreat towards recognizable intellectual property during challenging times. Familiar brands feel safer. They offer pre-sold awareness in a market where attention is fragmented and patience is scarce.

To some extent, that is exactly what is happening. Giant properties such as Yellowstone, Mission: Impossible, and Star Trek become even more strategically important. Yet the paradox is that even safe harbors can become too expensive to maintain in the form they took during the binge years.

Under Alex Kurtzman’s Secret Hideout, Star Trek produced an astonishing 251 episodes over roughly a decade. That output reflected a particular industrial logic: if the service needs feeding, the franchise must keep producing. But franchise saturation creates its own problems. Audience attention thins. Brand identity blurs.

So Star Trek is now doing something it has not done in years: it is slowing down.

For the first time in nearly a decade, there are no new live-action Star Trek series in active production. This is a fallow period, deliberate or otherwise, that suggests the franchise has reached the edge of what the old volume model could sustain. The retreat is financial, certainly, but it is also creative. A brand cannot renew itself if it is never allowed to stop performing.

Corporate Restructuring: The Layoff Crisis A report on the massive job cuts at Paramount as the studio pivot toward profitability.

When Tone Becomes Strategy

The most difficult part of the Star Trek story is not financial. It is tonal. For much of its history, Star Trek functioned as a kind of moral thought experiment. It addressed war, prejudice, and ethics through allegory.

That narrative contract changed over the last several years. Friction arose between inherited tone and current voice, and between a franchise built on speculative dislocation and writing that sometimes sounded as if it had been imported directly from the cultural vernacular of 2026.

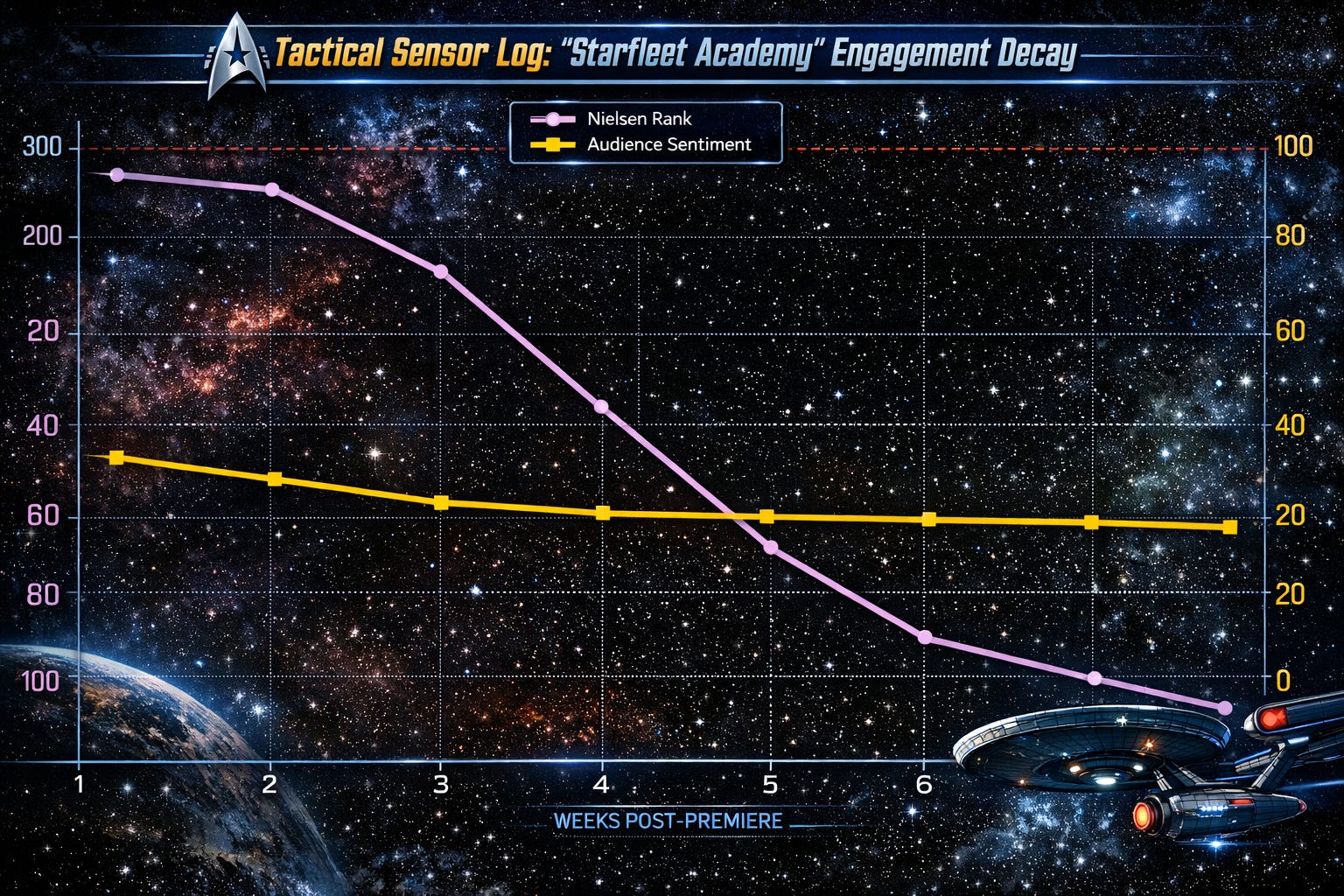

That friction reached a flashpoint with Star Trek: Starfleet Academy, which premiered on January 15, 2026. The problem, according to many critics and viewers, was that its version of renewal seemed to collapse the imaginative distance that gives science fiction its power. The 32nd century too often felt like a familiar present-day campus culture lightly draped in futuristic production design.

Once audiences feel that contract has been broken, the damage becomes commercial. Starfleet Academy reportedly drew about 2.1 million viewers in its first eight days, but enthusiasm faded quickly. By March 2026, Paramount announced that the series would end after its second season. If its cost truly approached 20 million dollars per episode, the margin for ambivalence was always going to be vanishingly thin.

The Death of the Streaming Side Quest

The reset extends beyond television. For years, studios flirted with the idea that direct-to-streaming films could expand a franchise without theatrical expectations. The release of Star Trek: Section 31 in January 2025 helped end that experiment. Landing at a grim 21% on Rotten Tomatoes, the film’s failure clarified the strategy: the future is no longer built around streaming side quests. It is being built around a hard reset.

The Kelvin Timeline films now appear effectively finished. In their place, Paramount and Skydance are pursuing a theatrical strategy. One project, directed by Toby Haynes, is an “origin” prequel focused on first contact. Another, from Jonathan Goldstein and John Francis Daley, is conceived as a fresh reboot with an entirely new cast.

The Future of the Final Frontier: Movie Reboot News Breaking down the latest developments on the Goldstein and Daley Star Trek film project.

Nostalgia, but Make It Asset-Light

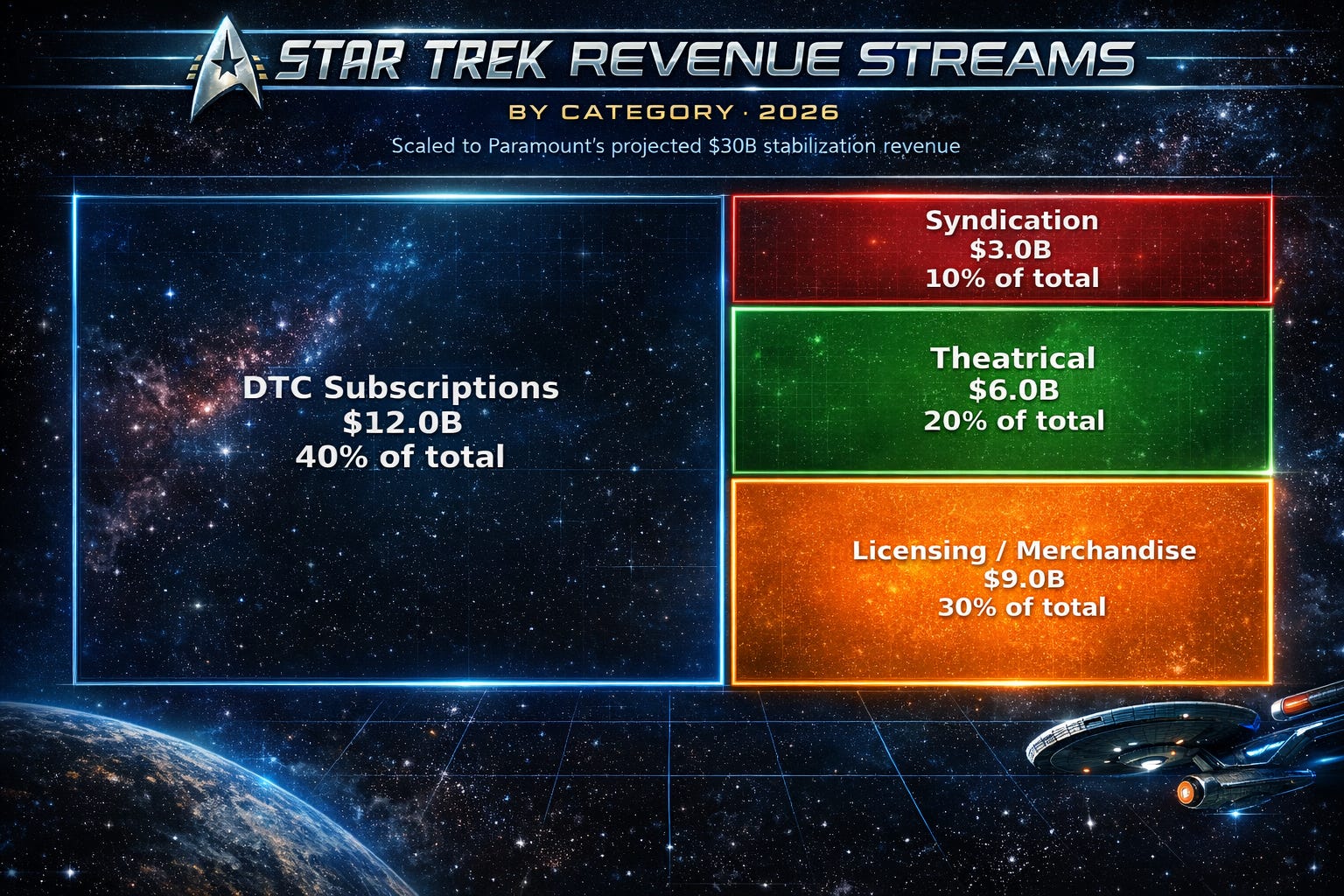

In a lower-growth entertainment economy, the expensive prestige series is no longer the only way to keep a brand culturally active. Audio dramas, digital comics, and merchandise extensions offer lower overhead.

The approaching 60th anniversary in 2026 sharpens this strategy further. LEGO partnerships and environmental campaigns allow the franchise to remain visible and monetizable while larger questions about its screen future are still being resolved. In the old model, licensing sometimes felt secondary; in the new one, it looks intelligent.

What Hollywood Has Learned

The streaming era encouraged a dangerous confusion between motion and health. The Great Deleveraging is what happens when numeracy catches up. Paramount’s effort to regain investment-grade debt metrics by the end of 2027 is part of that broader reckoning.

In one sense, this is a story about decline. In another, it is a story about rediscovery. Hollywood may be relearning a truth it spent a decade trying to outrun: that constraint is not the enemy of creativity. Sometimes it is the precondition for it.

At Paramount, beneath the famous water tower, the question is no longer how do we make more? It is why are we making this at all? The business is no longer organized around dreams of infinite expansion. It is organized around an audit. And that may be the most important plot twist in Hollywood: after years of trying to imagine the future, the industry has been forced to reckon with the cost of the story it told itself in the present.