The Hectocorn Ascent

How Private Giants Are Rewriting Sovereignty in an Era of Resource Bankruptcy

In California’s San Joaquin Valley, the old language of abundance is giving way to the harder language of limits. For decades, growers, districts, and communities operated under the assumption that they could pump, replace, and normalize groundwater according to the demands of modern agriculture.

It cannot. Under California’s Sustainable Groundwater Management Act (SGMA), much of the southern Central Valley is now being forced toward explicit groundwater budgets and sustainable-yield constraints after running an annual overdraft of roughly 2 million acre-feet for years. This is not just a regional water story. It is a preview of a broader civilizational adjustment: modern systems are increasingly being managed not for a return to old baselines, but for survival under permanent constraint.

That shift now has a name. On January 20, 2026, the United Nations University released its flagship report, “Global Water Bankruptcy: Living Beyond Our Hydrological Means in the Post-Crisis Era,” arguing that large parts of the world have moved beyond episodic water “crisis” and into a chronic condition of hydrological overshoot. A crisis implies interruption; bankruptcy implies that the books no longer work. Nearly 4 billion people face severe water scarcity for at least one month each year. Once a system reaches that point, the governing question changes: not how to restore the old equilibrium, but how to manage decline, allocate scarcity, and preserve continuity.

“A crisis implies interruption; bankruptcy implies that the books no longer work.”

That is where this story stops being only about water.

Bankruptcy, in any domain, has a political consequence: it changes who matters. When the public sector can no longer reliably provision what citizens and institutions cannot live without, power migrates toward whoever still can. In the 20th century, sovereignty was primarily expressed through territory, law, force, and taxation. In the 21st, it is increasingly expressed through infrastructure, computation, coordination, and control over defaults. The decisive actors are often not those who govern a map. They are those who can keep the system running when the map no longer guarantees order.

That is the real significance of the hectocorn.

A hectocorn is a private company valued at $100 billion or more. The label sounds like venture-capital theater, but it points to a structural change. These firms are no longer simply large businesses with successful products. They are becoming system operators, managing communications, payments, data, logistics, identity, intelligence, and the architecture through which entire sectors function. Valuation is not the same as sovereignty: GDP measures annual output; valuation discounts expectations of future cash flows, dominance, and strategic position. But the comparison is revealing because it captures the scale at which certain private firms now sit, not as market participants inside the system, but as layers the system increasingly depends on.

SpaceX: Orbital Sovereignty

No company illustrates that transition more vividly than SpaceX.

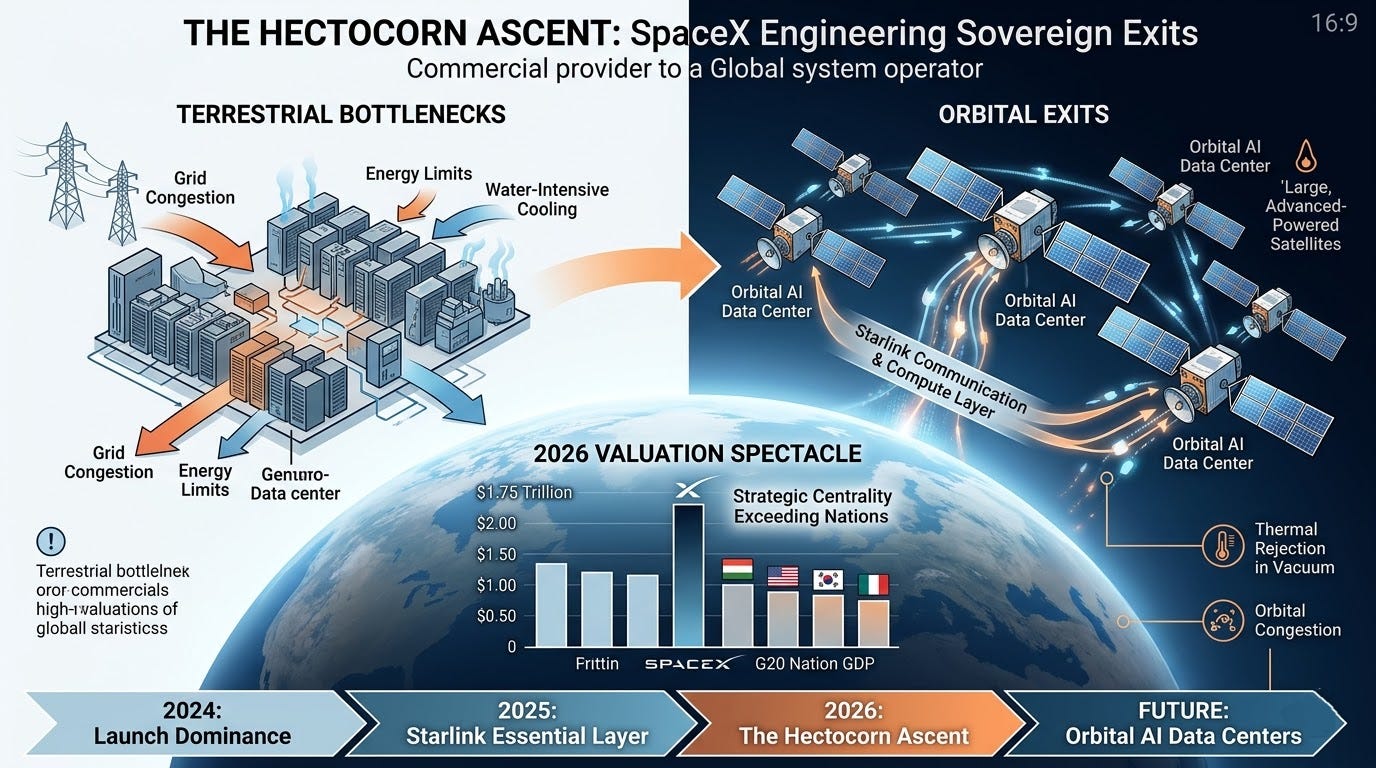

Reports from late February 2026 indicated SpaceX was aiming for a confidential IPO filing as soon as March, targeting a valuation over $1.75 trillion. On paper, those numbers are a financial spectacle. In practice, they imply something more profound: investors are treating a private company’s infrastructure as strategically central on a scale once reserved for nations.

SpaceX dominates launches and has made Starlink an essential communications layer, deeply embedded in defense, telecom, and orbital access. But the more revealing ambition is its pursuit of orbital data centers. SpaceX has sought FCC approval for up to one million solar-powered satellites configured as orbital AI data centers. The logic is clear: move critical compute away from terrestrial bottlenecks (grid congestion, energy limits, water-intensive cooling) toward abundant solar power in space. The concept is audacious. Engineering challenges include thermal rejection in vacuum and orbital congestion. Yet that is precisely the point: the most consequential private companies are no longer merely inventing products. They are engineering exits from public bottlenecks that states have proven too slow, fragmented, or capital-constrained to solve.

OpenAI: The Cognitive Layer

If SpaceX represents an infrastructure layer, OpenAI increasingly resembles an administrative one.

On February 27, 2026, OpenAI announced a $110 billion funding round, led by Amazon ($50 billion) with Nvidia and SoftBank ($30 billion each), at an $840 billion post-money valuation. The company also reported ChatGPT surpassing 900 million weekly active users. These are not product metrics. They describe a platform embedded in how people write, search, code, reason, and operate institutions. A generation ago, administrative power was visible in ministries. Today, some of it migrates into foundation-model platforms that mediate cognition itself.

The Financial Rails and the New Map

The same pattern appears in finance, where the question is not who prints money, but who controls the rails. In March 2026, Revolut secured its full UK banking license at a $75 billion valuation. Weeks earlier, Stripe reached $159 billion, reporting $1.9 trillion in total payment volume for 2025, roughly 1.6% of global GDP.

This is operational sovereignty: power belongs not to the decree-writer, but to the rail-controller everyone must use.

Conclusion: The Governance Signal

The World Economic Forum’s Global Risks Report 2026 captures the mood: near-term geopolitical risks dominate, pushing environmental concerns lower in priority. Into that gap step companies building around constraint.

Water bankruptcy is a governance signal. Once scarcity is chronic, the institutions that thrive are the functional ones, those delivering continuity when public baselines fracture. Hectocorn valuations price future dependence.

But history shows what happens when private systems become central enough that their failure socializes risk. The logic spreads: compute, communications, payments. Beneath the spectacle lies the question: Who governs the governors when they are platforms? Who absorbs the debt when new sovereign layers, built to manage scarcity, discover they too are overdrawn?

The era of water bankruptcy has arrived. The era of platform sovereignty arrives with it. The first warns of limits; the second scrambles for control over what remains. The map is no longer the whole story. The real borders of the next decade may be drawn around private systems deciding access to compute, capital, and continuity when old guarantees run out.