The Sovereignty Gap

Why the SpaceX IPO Says More About Modern Power Than Markets

In the winter of 1911, the United States Supreme Court issued its landmark ruling to break up John D. Rockefeller’s Standard Oil. The decision under the Sherman Antitrust Act was not triggered simply because the company was large but because it had engaged in specific, anti-competitive actions to maintain an over 90 percent market share in oil refining. The ruling reasserted a fundamental principle of twentieth-century governance: the state retains the ultimate authority to dictate the ground rules of public commerce.

That historic exercise of antitrust power relied on a geographical assumption that we rarely consider today. Standard Oil’s empire was made of dirt, steel, and iron. It consisted of physical pipelines dug into the soil of Ohio, refineries on the riverbanks of New Jersey, and rail cars rolling over American tracks. When a federal judge issued an injunction, marshals could physically walk onto the property to enforce it. Power was rooted in the ground.

If Space Exploration Technologies Corp. (SpaceX) proceeds with its planned June 12, 2026, public listing, that geographical assumption will face a distinct structural test.

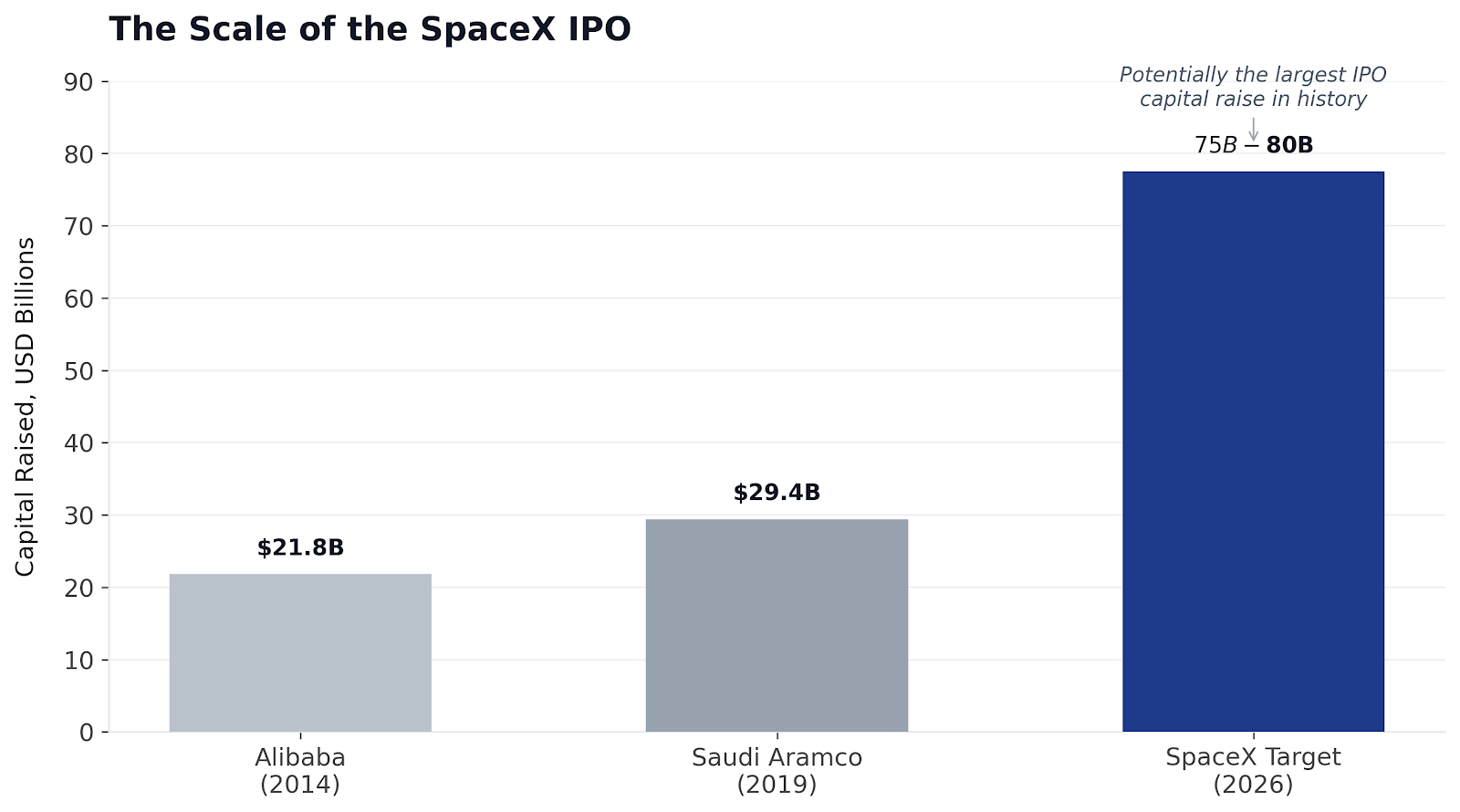

For months, Wall Street has focused on the staggering mechanics of the transaction. According to the Form S-1 registration statement filed with the Securities and Exchange Commission on May 20, 2026, the company is targeting a valuation range drifting between $1.75 trillion and $2.0 trillion, with a potential capital raise of $75 billion to $80 billion. Financial analysts have noted that under a tailored Nasdaq “Fast Entry” rule change, the company will be eligible to join the Nasdaq-100 index within 15 trading days of its debut. Some investment analysts warn that this rapid indexation could force passive funds to buy more than $50 billion of SPCX shares within two weeks, creating localized selling pressure elsewhere in large-cap tech.

Those questions matter for portfolios. But the more compelling story lies in what the prospectus reveals about a shifting political economy.

The strategic implication is that SpaceX is not challenging the state by replacing it; it is challenging the state by becoming infrastructure the state cannot easily function without. The company has moved beyond the traditional boundaries of a standard aerospace contractor to sit at the intersection of launch systems, satellite communications, military logistics, and AI infrastructure. SpaceX remains dominant, but competitors including Blue Origin, Amazon’s Project Kuiper, Chinese sovereign constellations, and emerging European launch initiatives are attempting to reduce that dependence. Yet, for the immediate future, the company has achieved a degree of dominance where regulators increasingly find themselves acting as dependent customers.

The Speed Inversion

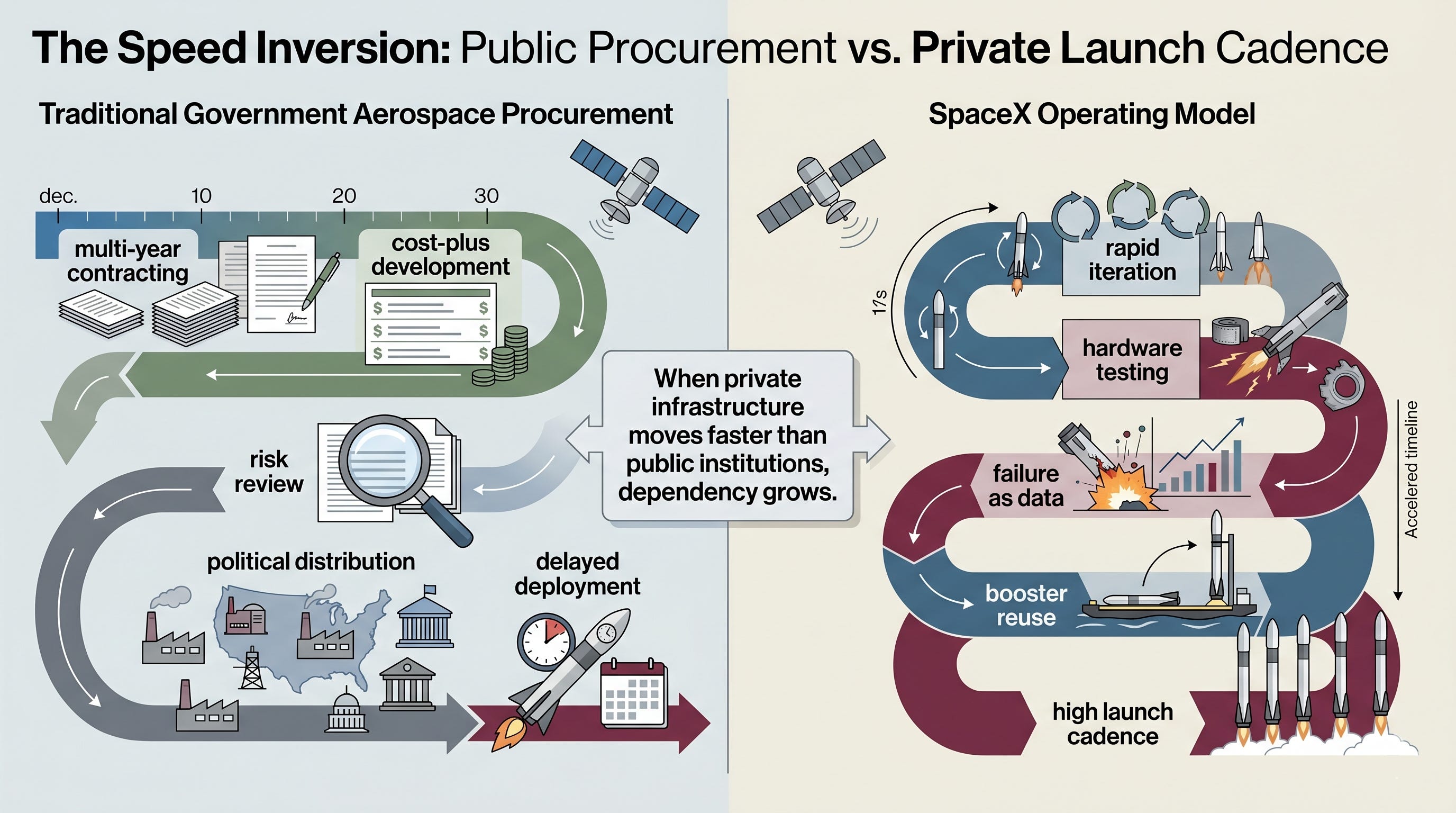

The current friction between public regulatory agencies and private aerospace speed is best understood through the lens of institutional velocity.

For decades, government space procurement operated on a deliberate, heavily managed rhythm. Large government contractors worked within defense acquisition systems optimized for multi-year cost-plus contracts, stability, and the political distribution of manufacturing across multiple congressional districts. While this structure minimized certain operational risks, it also created procurement timelines that struggled to adapt to rapid technological shifts.

SpaceX operated on a different set of institutional assumptions. The company tolerated engineering failure publicly, iterated aggressively on hardware, and concentrated decision-making authority. The approach initially drew skepticism from legacy aerospace veterans, but it ultimately yielded significant operational advantages.

The S-1 filing states that SpaceX has successfully launched more than 80% of all payload mass to orbit globally in each year since 2023. The Falcon 9 has achieved a 99% plus mission success rate, altering the economics of orbital access through booster reusability.

The political implication is that a profound speed inversion has occurred. The irony is difficult to miss: governments that once dismissed reusable rockets as fantasy are now structurally dependent on them. When a private contractor operates at a velocity that outpaces public bureaucracy, the state can find its own internal technical capacities hollowed out.

According to the filing, SpaceX currently holds more than $24.4 billion in active federal contracts spanning NASA, the Air Force, and the Space Force. This structural reliance is not abstract. Federal procurement disclosures reveal that modern deployment frameworks, tactical communications, and satellite-guided tracking systems are deeply dependent on commercial infrastructure networks. When defense networks face localized server disruptions or physical connection failures, tactical units rely on private corporate constellations in low-Earth orbit to maintain vital video and data transmission links.

Ukraine Says Russia Is Using Starlink: How Elon Musk’s Satellites Work

The Realistic Limits of Orbital Compute

The company’s long-term valuation case relies heavily on the February 2026 all-stock merger with xAI, which integrated Elon Musk’s artificial intelligence assets directly under SpaceX control. The prospectus details a forward-looking roadmap to begin deploying space-based AI data centers as early as 2028, seeking regulatory approval to launch up to one million satellites to function as a data center network. Industry analysts remain divided on whether deployments at that scale are technically or politically feasible.

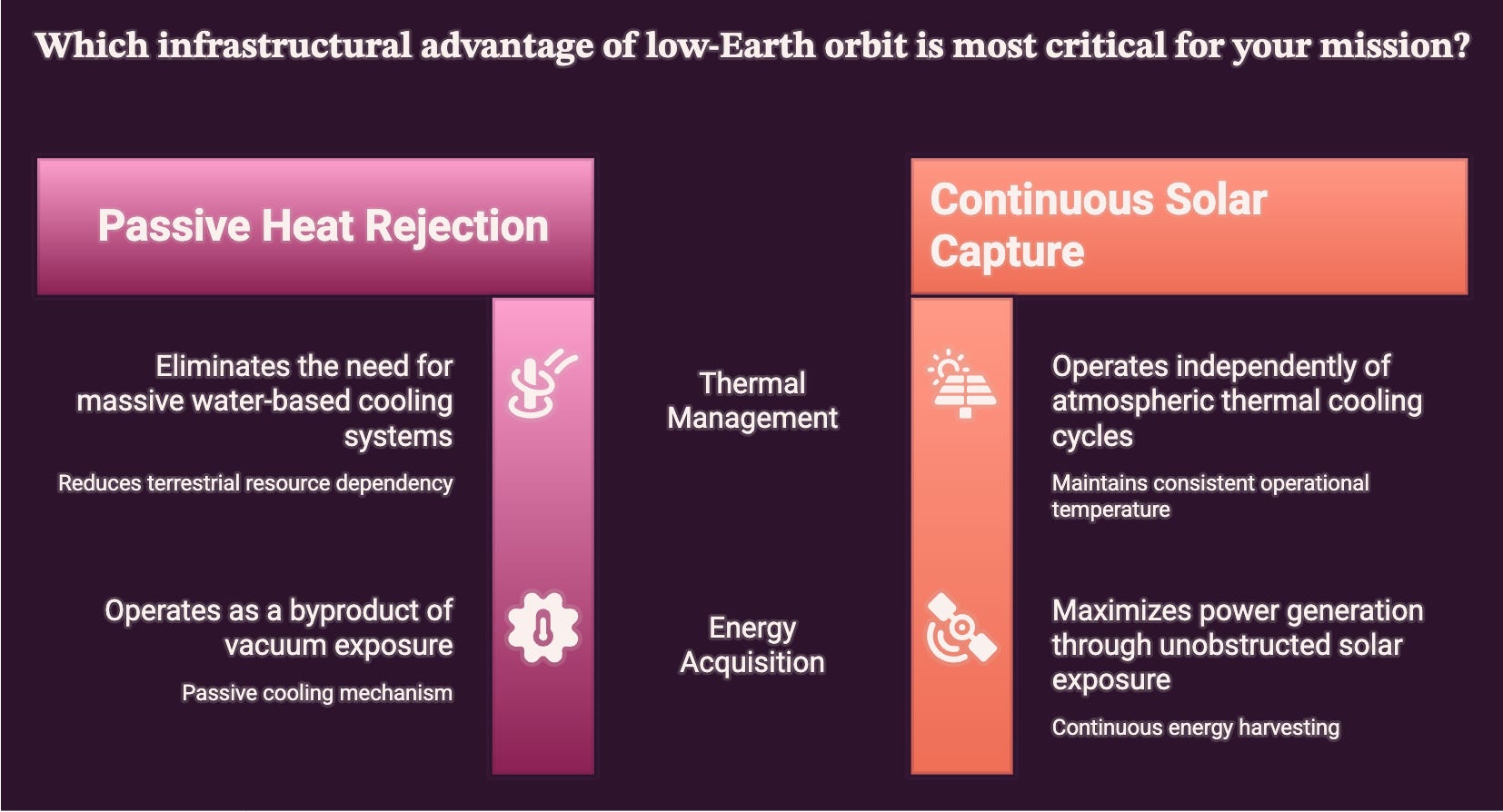

The corporate thesis is that low-Earth orbit offers distinct infrastructural advantages:

Passive Heat Rejection: Utilizing thermal radiation into the vacuum of space, reducing the massive water and cooling dependencies required on land.

Continuous Solar Capture: Solar arrays positioned above atmospheric interference can capture continuous solar radiation.

However, the technical section of the prospectus also reveals a daunting list of real-world obstacles that complicate this vision. Many aerospace engineers remain skeptical that orbital compute can economically outperform rapidly improving terrestrial AI infrastructure. The concern is that these factors may represent severe operational headwinds rather than a guaranteed technological leap.

SpaceX Wants to Blast Data Centers Into Orbit. Here’s What It May Take

First, there is the problem of radiation hardening. Terrestrial silicon chips are highly vulnerable to cosmic rays and solar flares, requiring heavy, expensive shielding or redundant software architectures to prevent computational bit flips. Second, hardware repair is physically impossible at scale once a satellite is deployed; if an AI processor fails, it becomes immediate space debris. Third, the replacement cycles for low-Earth orbit satellites are short, typically five to seven years, requiring a continuous, high-cost launch cadence just to maintain the computational network’s baseline capacity.

Furthermore, there are significant latency tradeoffs. While light travels faster through the vacuum of space than through terrestrial fiber-optic cables, the physical distance between an orbital data center and a ground station introduces lag that may make real-time, high-frequency AI inference uncompetitive compared to localized edge processors. These computing constellations also face immense power storage hurdles, requiring heavy, next-generation battery arrays to sustain intense processing loads when passing through the Earth’s shadow.

The Contradictions of Governance

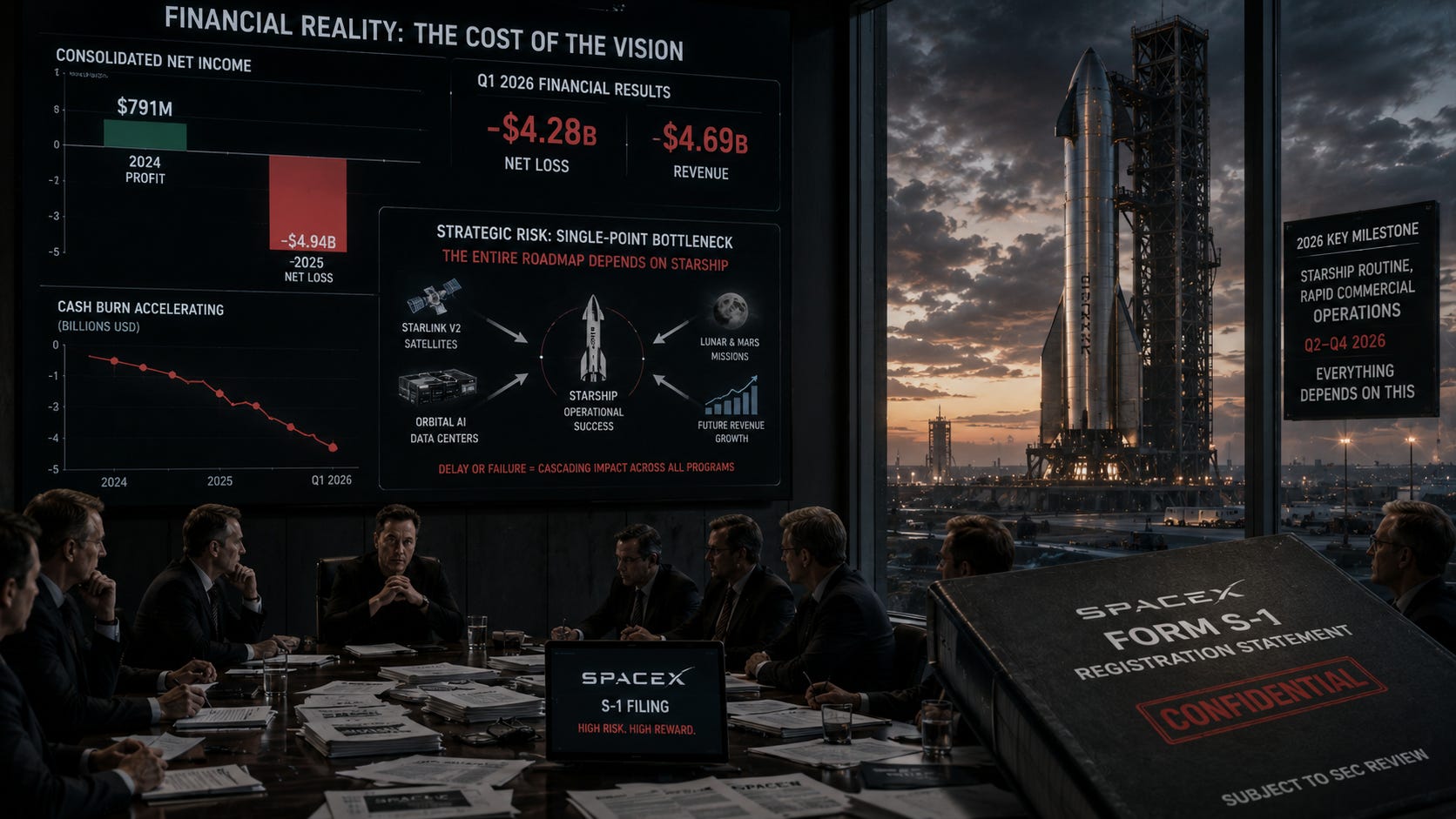

The S-1 filing lays bare the severe financial strain of attempting to build this frontier infrastructure. SpaceX absorbed xAI’s massive cash burn rate, which pulled the consolidated bottom line from a $791 million profit in 2024 down to a staggering $4.94 billion net loss for 2025. The financial hemorrhage accelerated into the first quarter of 2026, which posted a single-quarter net loss of $4.28 billion on revenue of $4.69 billion.

The strategic risk is that the company’s entire forward roadmap depends on a single-point operational bottleneck: the Starship launch platform. Every projection, from deploying larger Starlink V2 satellites to launching the 2028 orbital data centers, relies on Starship achieving routine, rapid commercial operations in the second half of 2026.

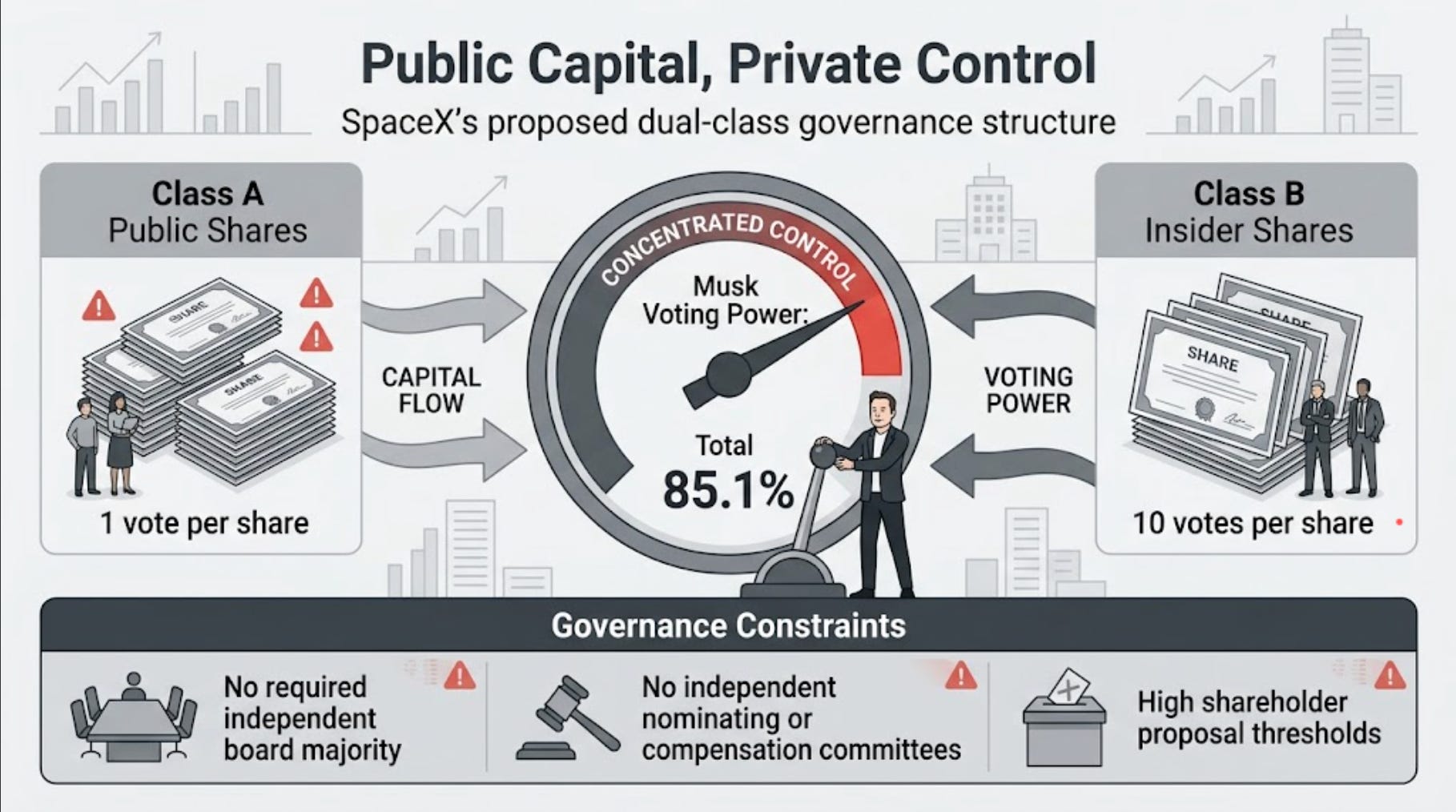

Yet, while public markets are being asked to absorb these losses and risks, the corporate governance framework ensures that public investors have practically no mechanism to influence the company’s direction. Legal analysts tracking the listing note that the company’s internal command structure functions essentially without public oversight. Through a dual-class share architecture where Class B common stock carries ten votes per share to Class A’s one, Elon Musk retains 85.1% of the total voting power.

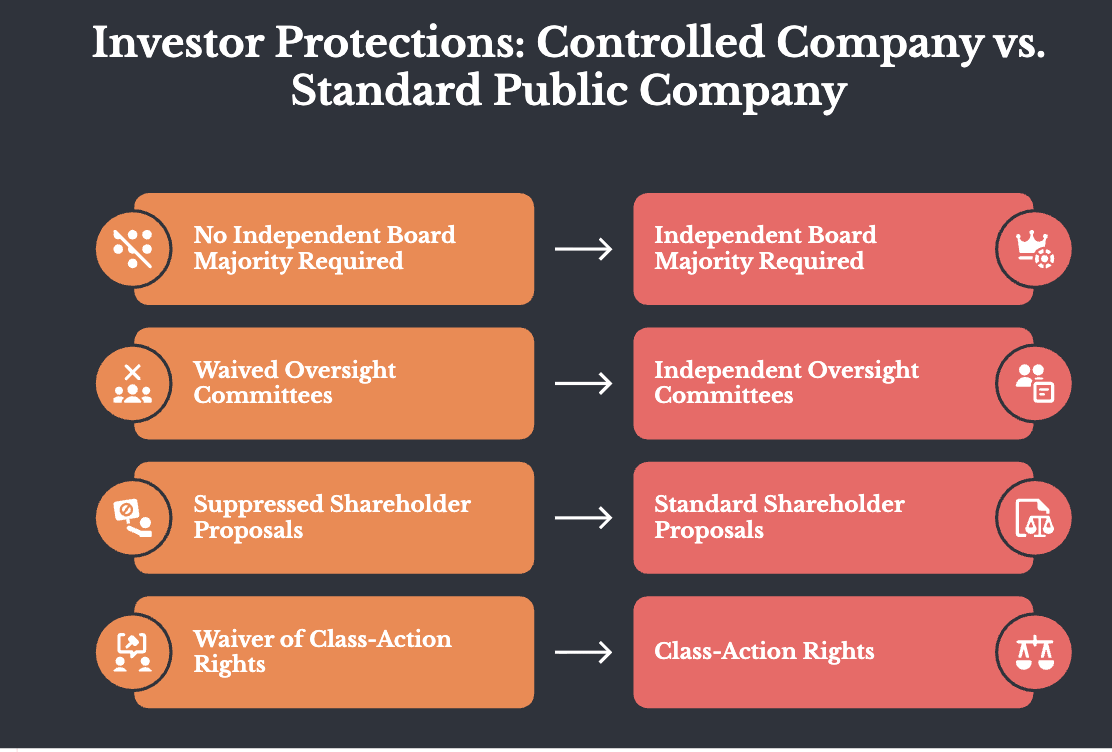

Because SpaceX has claimed the “Controlled Company” exemption under Nasdaq rules, standard public investor protections have been significantly limited:

No Independent Board Majority: The nine-member board is not required to maintain a majority of independent directors.

Waived Oversight Committees: The company has declined to adopt independent nominating or compensation committees.

Suppressed Shareholder Proposals: Raising an operational proposal requires an unusually high minimum holding of 3% of voting shares held for six months, alongside a 67% proxy solicitation requirement.

Waiver of Class-Action Rights: Derivative litigation requires a baseline of 3% of outstanding common stock and enforces a class-action waiver.

The corporate governance structure means that public capital is being engineered to fund a private, founder-driven strategic vision that is entirely insulated from short-term public market or shareholder pressure. History suggests that concentrations of power eventually invite counterforces, but whether that transition ultimately succeeds remains an open question.

The Sovereign Counter-Response

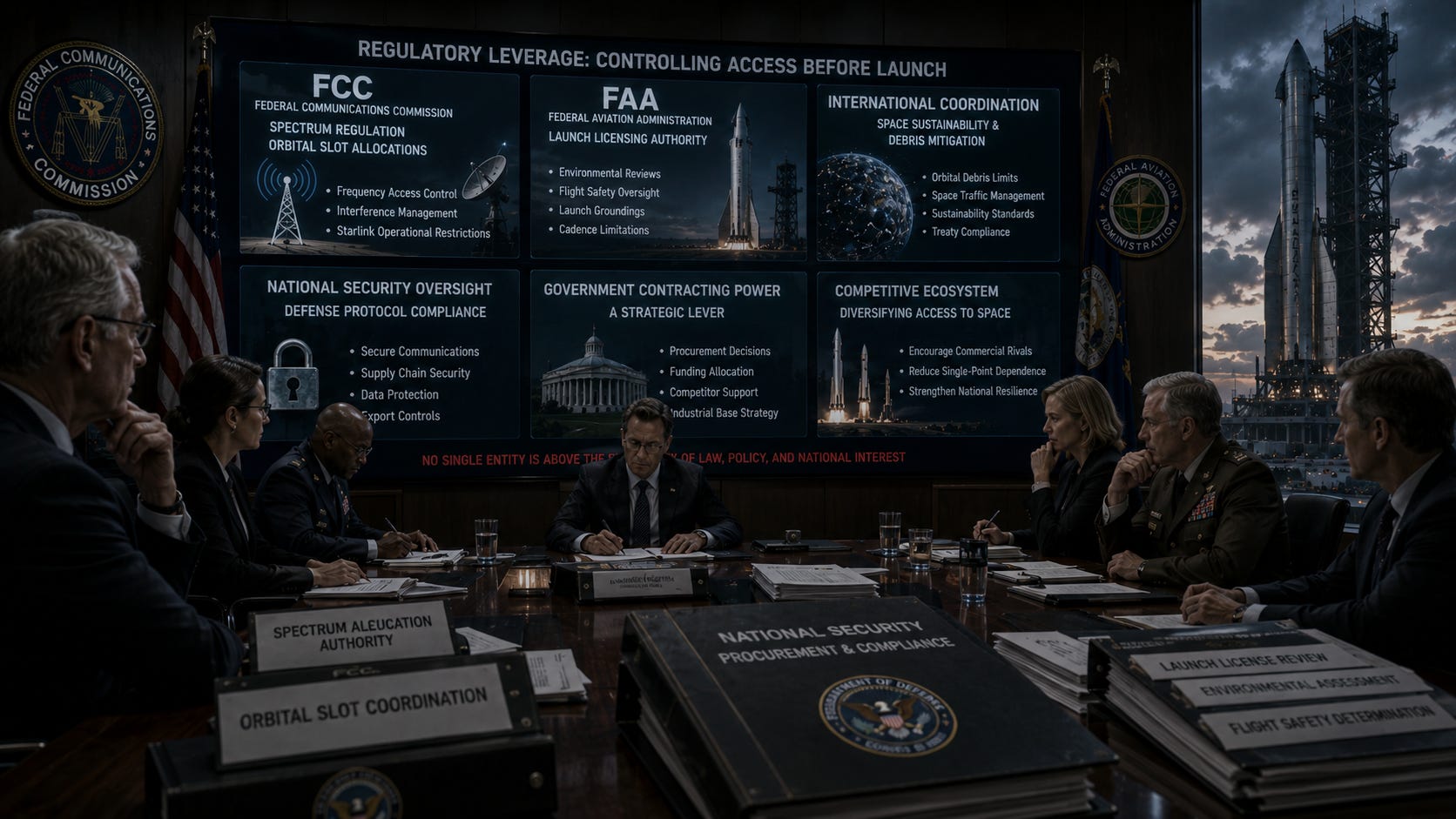

It would be a mistake, however, to view the state as completely paralyzed. A robust set of competing international perspectives and regulatory tools suggests that the balance of power remains contested.

The unresolved question is how effectively the state will deploy its traditional levers. While SpaceX operates as a dominant player in Western satellite broadband, it faces an accelerating sovereign counter-response globally. China is actively investing in its own massive, state-backed low-Earth orbit constellations, such as the G60 Starlink and the Guowang network, explicitly designed to ensure space infrastructure remains under national, centralized authority.

Why Europe is Creating an Alternative to Starlink

Telecommunications regulators retain the structural leverage to limit the company’s operational reach before it ever reaches orbit. Domestically, the Federal Communications Commission maintains control over spectrum regulation and orbital slot allocations, and it can restrict the radio frequencies required for Starlink to operate. The Federal Aviation Administration can impose strict environmental reviews and flight groundings, creating an immediate regulatory bottleneck for Starship launch cadences.

Furthermore, international bodies are increasingly leveraging orbital debris limits and space sustainability laws to restrict the sheer volume of satellite deployments. The state’s government contracting power also cuts both ways; national security laws require strict compliance with defense protocols, and the Department of Defense can alter its procurement strategies to deliberately fund and cultivate commercial competitors.

Antitrust tools are also far from obsolete. While a globally integrated satellite network does not fit neatly inside standard twentieth-century territorial laws, the Department of Justice and the Federal Trade Commission still possess the authority to review related-party transactions, restrict anticompetitive tying arrangements between launch and satellite services, or mandate structural separation if commercial dominance threatens domestic security.

The Reality of the Frontier

The broader market fascination with the SPCX prospectus reflects a growing recognition of this structural tension. We are witnessing a clear inflection point in the relationship between public authority and private execution.

The ultimate takeaway of this orbital transition is a historical reversal. For the past century, the social contract dictated that the state stood firmly above industry to regulate corporate behavior on behalf of the citizen. Today, the balance has shifted. Governments are looking to a singular corporate entity to keep them from falling into strategic and technological obsolescence. When a state relies on a private entity to launch its intelligence networks, secure its military communications, and pioneer its computational infrastructure, the traditional leverage of democratic governance is structurally altered.

The risk is that markets evaluate the offering primarily through short-term financial metrics while overlooking these deeper structural shifts. Investors are analyzing a listing through the sanitized language of price-to-sales multiples and index rebalancing flows. Public institutions are now facing the structural limits of enforcement after years of outsourcing core technical capacity to commercial providers. If a democracy treats its most vital twenty-first-century infrastructure as a mere commercial service, it must prepare for the long-term political consequence: a system where the line between regulator and customer disappears entirely.

When the opening bell rings, Wall Street will focus on the immediate trading volume, index rebalancing, and the financial multiple. Retail investors will buy into the vision of a multiplanetary future.

But underneath the market noise, the larger story is already taking shape. The old monopolies were rooted in the ground. This one is moving overhead.